What does rollover IRA activation mean?

Isabella Wilson

Isabella Wilson

A Rollover IRA is an account that allows you to move funds from your old employer-sponsored retirement plan into an IRA. With an IRA rollover, you can preserve the tax-deferred status of your retirement assets, without paying current taxes or early withdrawal penalties at the time of transfer.

Can I take a tax loss on rollover IRA?

You can’t take IRA investment losses as a capital loss. Instead, you claim IRA investment losses as a miscellaneous deduction, subject to the 2 percent income exclusion. You must add your IRA loss to all of your other miscellaneous deductions.

When must a tax free IRA rollover contribution generally be made?

60 days

You have 60 days from the date you receive an IRA or retirement plan distribution to roll it over to another plan or IRA. The IRS may waive the 60-day rollover requirement in certain situations if you missed the deadline because of circumstances beyond your control.

Can you lose money in a IRA?

An IRA is a type of tax-advantaged investment account that may help individuals plan and save for retirement. IRAs permit a wide range of investments, but—as with any volatile investment—individuals might lose money in an IRA, if their investments are dinged by market highs and lows.

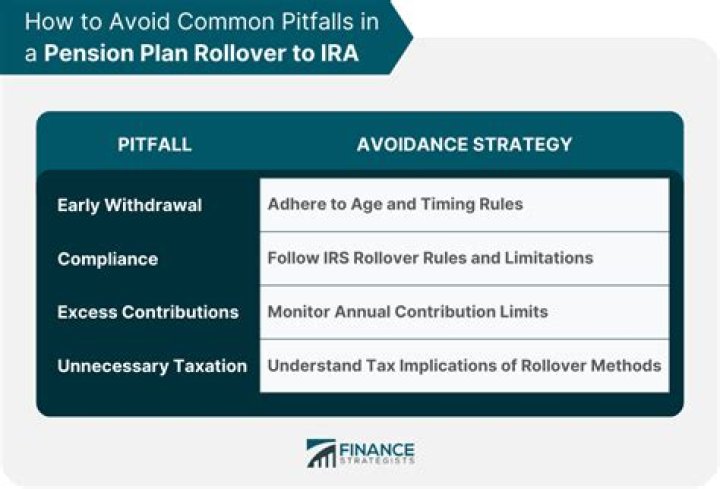

What are the penalties for making an ineligible rollover to an IRA?

Excess Contribution Penalties. If you make an ineligible rollover, you have to treat the contribution to the IRA as part of your annual contribution, subject to your annual contribution limits. For example, if your annual contribution limit is $6,000 and you contribute $10,000 of an ineligible rollover, you’ve made an excess contribution of $4,000.

What kind of rollover funds can I roll over to a traditional IRA?

You can rollover funds from any of your own traditional IRAs, but you can also roll over funds to your traditional IRA from the following retirement plans: 1 A traditional IRA you inherit from your deceased spouse 2 A qualified plan 3 A tax-sheltered annuity plan 4 A government deferred-compensation plan ( section 457 plan)

How long does it take to roll over from one IRA to another?

The 60-Day Rule. After you receive the funds from your IRA, you have 60 days to complete the rollover to another IRA.

Do you have to roll money from IRA to qualified plan?

Your employer is not required to accept such rollovers, so check with your plan’s administrator before you distribute the assets from your IRA. Certain amounts, such as nontaxable amounts and RMDs, cannot be rolled from an IRA to a qualified plan. Investopedia requires writers to use primary sources to support their work.