What happens if a CPA makes an error on a tax return?

Sophia Bowman

Sophia Bowman

If the client decides not to correct the error, SSTS No. 6 advises the CPA to consider whether to terminate the client relationship, as it could indicate issues with the client’s integrity. The CPA may also consider withdrawing from the engagement if the tax return cannot be prepared without perpetuating the error made on the prior – year return.

What to do if a tax preparer makes an error?

Regulation of independent tax preparers is lax in most states. Accountants, lawyers, and enrolled agents are highly qualified for the job of tax preparation. If you find an error in your taxes, file an amended return as soon as you can. If you suspect misconduct on the part of your preparer, file a complaint with the IRS.

What should I do if I made a mistake on my tax return?

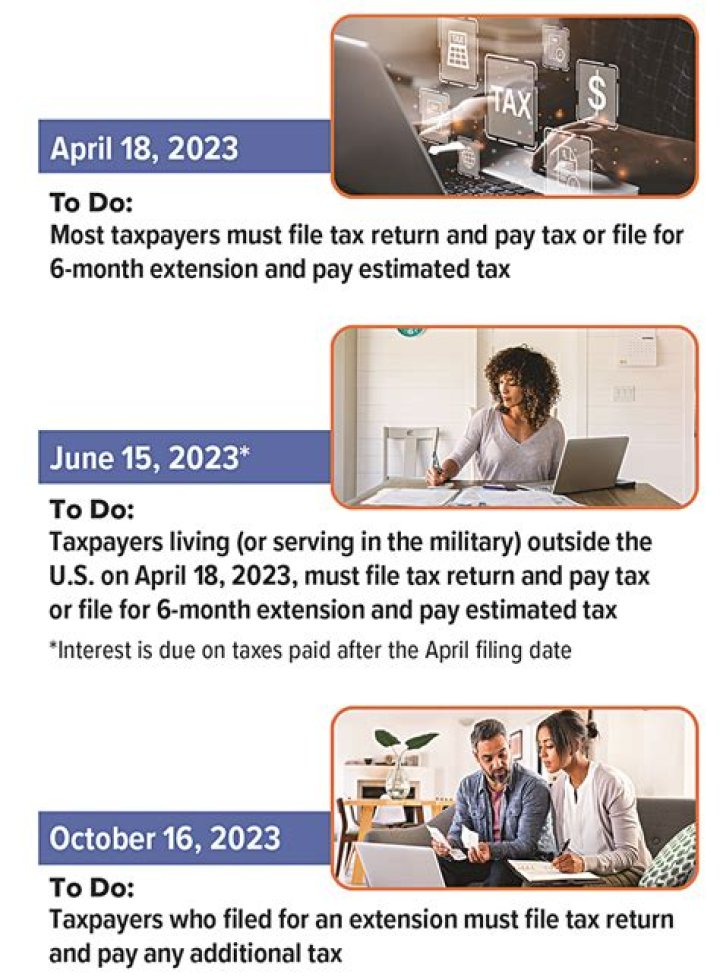

Taxpayers who discover they made mistakes or omissions on their tax return can correct them by filing an amended tax return. Those who need to amend should remember these tips: File using paper form. Use Form 1040X, Amended U.S. Individual Income Tax Return, to correct the tax return. Taxpayers can’t file amended returns electronically.

Are there any errors on state tax returns?

Furthermore, the former preparer did not include an addition modification for bonus depreciation on the client’s state income tax return. Both errors resulted in a significant understatement of taxable income.

Quantify the impact on the amount of taxes due for any prior-year return affected by the error or omission. A client’s ability to comprehend the consequences of an error and of a failure to remedy it depends in part on an understanding of the financial exposure for any tax understatement.

Who is David w.klasing esq.cpa M.S.Tax?

David W. Klasing Esq. CPA M.S.-Tax has earned dual California licenses that enable him to simultaneously practice as an Attorney and as a Certified Public Accountant in the practice areas of Taxation, Estate Planning and Business Law.

What causes a CPA to make an omission?

Determine the cause of the error or omission. Errors may result from weak accounting systems or lax internal controls, miscommunication, or good-faith mistakes by the client or the CPA. Understanding the cause will help to avoid repeating the mistake by strengthening systems and controls or improving communication.

When does a CPA need to disclose a prior year error?

If the prior-year error could result in an understatement on the current or a future return, it may require a return disclosure or even prevent the CPA from preparing the current/future return under Sec. 6694 and Circular 230 §10.34.

When does a CPA fail to comply with a client request?

Under this section, when a client or former client requests that the client’s records either be sent to the client or forwarded to another CPA, a member’s failure to comply with the request would constitute a violation of this interpretation.

When does a CPA have a duty to notify the IRS?

While a tax practitioner and AICPA member has a duty, as described above, to notify the client, the client is responsible for deciding whether to correct the error. The CPA is not required to inform the IRS or other taxing authorities of the client’s error and can only do so with the taxpayer’s permission, unless otherwise required by law.

When does a CPA withdraw from an engagement?

The CPA may also consider withdrawing from the engagement if the tax return cannot be prepared without perpetuating the error made on the prior – year return. The exhibit below provides a summary of the rules under both Section 10.21 of Circular 230 and SSTS No. 6.

Is the CPA required to notify a client of an error?

Furthermore, as an AICPA member, the CPA is subject to Statement on Standards for Tax Services (SSTS) No. 6, Knowledge of Error: Return Preparation and Administrative Proceedings, which also requires the CPA to notify the client of the error or omission and potential consequences.

Who is responsible for correcting an error on a tax return?

While a tax practitioner and AICPA member has a duty to notify the client, the client is responsible for deciding whether to correct the error. This site uses cookies to store information on your computer. Some are essential to make our site work; others help us improve the user experience.

What should a CPA do to avoid repeating a mistake?

Not only should a CPA preparing the current-year return take reasonable steps to avoid repeating the mistake under SSTS 6; the existence of adequate processes for avoiding repetition of errors is a component of the reasonable cause defense in Regs. Sec. 1.6694-2 (d).

What happens if a client refuses to correct a prior year tax return?

First, if a client refuses to correct an error in a prior year and the erroneous item would continue to the current-year return, continuing to represent the client will lead to a situation where the tax practitioner’s professional obligations and the client’s interests will almost surely be on a collision course.

When is a tax preparer liable for an error?

Thus, for example, if a tax preparer committed an error–intentionally or unintentionally–on Forms 1040, 1040A, 1040EZ, 1041s, or 1065 (partnership) and 1041 (grantor trusts), the preparer was liable. Today, since 2007, a tax preparer will be liable for errors committed on any return.

What should I do if I have an error on my tax return?

Under AICPA Statement on Standards for Tax Services (SSTS) No. 6 and Circular 230, a tax practitioner who learns of an error in a client’s previously filed tax return must inform the client of the error and its consequences and (under SSTS No. 6) recommend corrective measures.