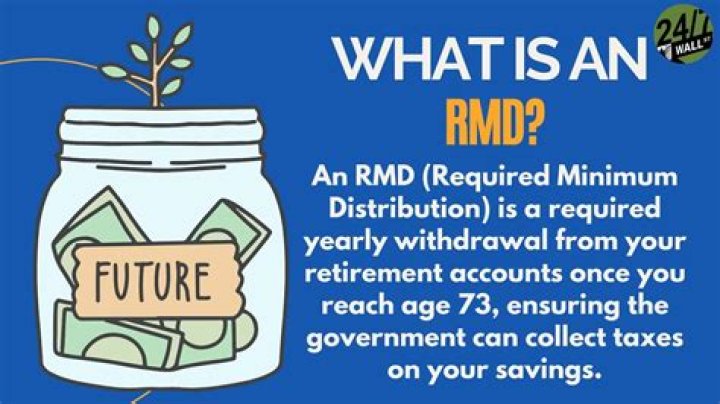

What happens if RMD is not taken in year of death?

Aria Murphy

Aria Murphy

If the year-of-death RMD was not already taken by the IRA owner, it must be taken by the beneficiary. It is not paid to the IRA owner’s estate, unless the estate is named as the beneficiary. By law, the minute the IRA owner dies, the balance in the IRA belongs to the beneficiary, NOT the estate.

Do you have to take an RMD in the year you die?

When an account owner dies before satisfying a required minimum distribution (RMD) for the year, the beneficiaries must distribute the remaining RMD amount by December 31 of the year of death. If a trust or estate is the IRA beneficiary, that entity is responsible for taking the year-of-death RMD.

Do I need to take a RMD in 2020?

You must take your first required minimum distribution for the year in which you turn age 72 (70 ½ if you reach 70 ½ before January 1, 2020). If you reach 70½ in 2020, you have to take your first RMD by April 1 of the year after you reach the age of 72.

Do you have to take RMD in year of death?

Instead, the spouse is required to take a required minimum distribution for that year, determined with respect to the deceased IRA owner under the rules of A–4(a) of §1.401(a)(9)–5, to the extent such a distribution was not made to the IRA owner before death.

When do you have to take RMD on inherited IRA?

RMDs are not just for those reaching age 70½. Non-spouse beneficiaries of traditional IRAs and Roth IRAs are required to begin taking RMDs for an inherited IRA or Roth IRA by December 31 st of the year after the year of the original owner’s death if they want to stretch RMDs over their life expectancy.

When to take a RMD before spousal rollover?

Husband passed away 2010 at age 76 before taking this year’s RMD on his traditional IRA. Wife is sole beneficiary, also 76. My understanding is that the wife has to take his RMD for 2010 before either assuming the account and treating it as her own, or rolling it over into a new account in her name.

What happens if you make a mistake on your RMD?

Unfortunately, though, the RMD rules can be maddeningly complicated, making it easy for taxpayers to make a mistake by taking a smaller-than-required distribution, taking a distribution from the wrong account (or even the wrong type of account), or (worse yet) missing a distribution altogether.