What happens if you Overcontribute to SIMPLE IRA?

David Craig

David Craig

Any amount contributed to your SIMPLE IRA above the maximum limit is considered an “excess contribution.” An excess contribution is subject to an excise tax of 6% for each year it remains in your SIMPLE IRA. An excess contribution may be corrected without paying a 6% penalty.

When can a SIMPLE IRA be rolled over?

You can only roll over money from your SIMPLE IRA once per 12-month period. If you take a second distribution from the SIMPLE IRA within 12 months, it is ineligible to be rolled over.

Can you do a 60 day rollover from a SIMPLE IRA?

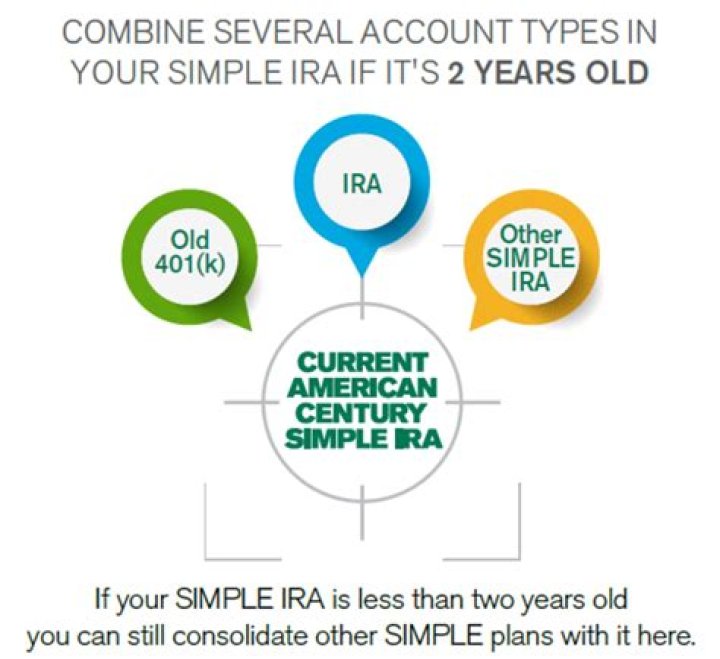

Yes, you can do a 60 day rollover out of a SIMPLE IRA and back in. You can also roll a SIMPLE IRA balance into another SIMPLE IRA without waiting for the 2 year period to end as you would have do if the rollover went into a different kind of plan.

Can a SIMPLE IRA be rolled over to a Roth IRA?

The IRS has established a number of simple IRA rollover rules. As previously mentioned, you are not able to complete a simple IRA rollover during the first two years from the date of your initial contribution to any other retirement account except a new simple IRA.

Is there an early distribution penalty for SIMPLE IRA?

These accounts function in a similar manner as 401 (k) plans. The annual contribution limits for employees to SIMPLE IRA accounts is $13,000 if they are younger than age 50 and an additional $3,000 per year if they are older than age 50. SIMPLE IRAs have an early distribution penalty of 10 percent for people who are younger than age 59 1/2.

What’s the annual contribution limit for a SIMPLE IRA?

The annual contribution limits for employees to SIMPLE IRA accounts is $13,000 if they are younger than age 50 and an additional $3,000 per year if they are older than age 50. SIMPLE IRAs have an early distribution penalty of 10 percent for people who are younger than age 59 1/2. There are also RMDs beginning after the owners turn age 70 1/2.

What is the age 55 rule for IRA withdrawals?

The age 55 rule applies to individuals who choose to terminate employment in the year of their 55th birthday or older and are thus eligible to take a distribution from a company retirement plan without being subject to the 10% penalty. This policy applies only to calendar years, not 365 days surrounding one’s 55th birthday.