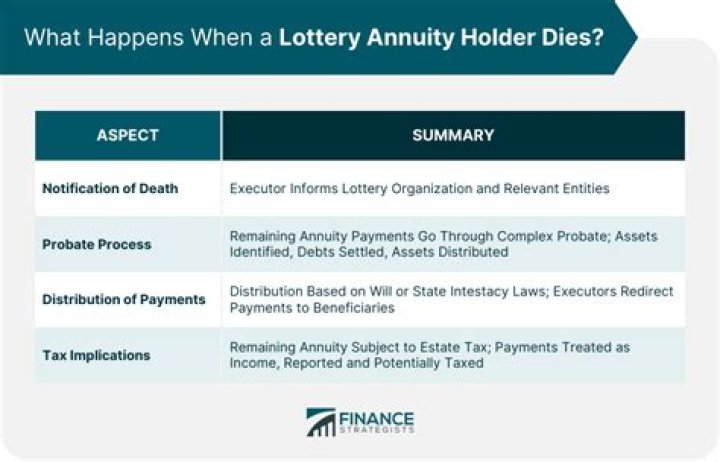

What happens to an inherited annuity after death?

Aria Murphy

Aria Murphy

Some annuities payments can be left to a beneficiary after death if money remains.

How does the five year rule work for inherited annuities?

A lump sum payment provides the beneficiary with the flexibility to pay off debt and larger expenses at one time. Five-Year Rule – The five-year rule requires the inherited beneficiary to receive the full distribution within five years of the annuitant’s death.

What kind of tax do you pay on an inherited annuity?

When a person inherits an annuity, the gains stay with the policy. Depending on the type of annuity, tax will have to be paid on the lump sum received or on the regular fixed payments. The payments received from an annuity are treated as ordinary income, which could be as high as 37% tax depending on your tax bracket.

Can a beneficiary of an annuity be a surviving spouse?

If an annuity contract has a death-benefit provision, the owner can designate a beneficiary to inherit the remaining annuity payments after death. Earnings on inherited annuities are taxable. How they’re taxed depends on the annuity’s payout structure and whether the beneficiary is the surviving spouse or someone other than the spouse.

Who is responsible for paying taxes on an inherited annuity?

The annuity beneficiary will be responsible for paying this estate tax. While receiving monthly, quarterly or yearly payments may be beneficial, some inherited annuitants may choose to sell their annuity to pay for emergency expenses, tuition, or to alleviate debt.

What happens if I inherit money from my mom?

So, if your mom dies and has $50,000 in her checking account or you find it stuffed under her mattress, you can receive that money and it’s not income to you (providing you are a beneficiary of her estate). This is true whether you inherit the money from a relative or a friend.