What happens when a trust is beneficiary of an IRA?

David Craig

David Craig

When a trust is named the beneficiary of an IRA, the trust typically receives the IRA proceeds upon the IRA owner’s death. The IRA is then a separate trust asset and should be held as a separate account. We will discuss later whether it is the trust, or the beneficiaries who will pay tax on the IRA proceeds.

Can a trust transfer an IRA to a trust beneficiary?

The simple answer is yes, in most cases a trustee can transfer an inherited IRA out of the trust to the trust beneficiary or beneficiaries without any negative tax consequences.

Who should be the beneficiary of an IRA?

A beneficiary can be any person or entity the owner chooses to receive the benefits of a retirement account or an IRA after he or she dies. Beneficiaries of a retirement account or traditional IRA must include in their gross income any taxable distributions they receive.

Should trust be beneficiary of IRA?

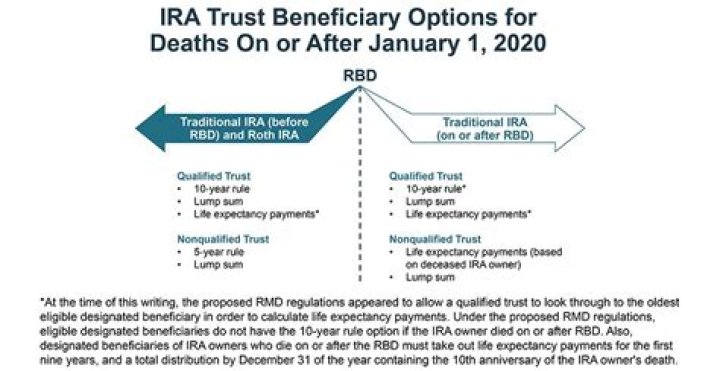

However, a trust also can be named as an IRA beneficiary, and in many instances, a trust is a better option than naming an individual. When a trust is named as the beneficiary of an IRA, the trust inherits the IRA when the IRA owner dies. The IRA then is maintained as a separate account that is an asset of the trust.

Can a trust be established as a beneficiary of an IRA?

In general, the exception applies if the following requirements are met: The trust is valid under state law. The trust is irrevocable or will, by its terms, become irrevocable upon the death of the IRA owner. The beneficiaries of the trust are identifiable.

Can a wife be the sole beneficiary of a trust?

The wife had previously established the trust and was the sole beneficiary and sole trustee of the trust. She could amend or revoke the trust and could distribute all income and principal of the trust for her own benefit. In effect, it was a standard revocable living trust that is primarily used to avoid probate.

How is a Conduit Trust different from an IRA?

It is considered a “conduit trust,” as the trust’s existence is ignored for the purpose of identifying a classification of the beneficiary. For example, if the beneficiary identified by the trust is an estate or charity (a non-person entity), the IRA is treated as having no designated beneficiary.

Can a primary beneficiary of a trust disclaim the assets?

The trust is eligible to disclaim the assets. If this happens, the other primary or contingent beneficiary usually inherits the assets, and the provisions of the trust no longer apply. This can be avoided by including a ‘disclaimer provision’ in the trust.