What income is subject to Ubti?

Aria Murphy

Aria Murphy

Unrelated business taxable income

Unrelated business taxable income (UBTI) is income regularly generated by a tax-exempt entity by means of taxable activities. UBTI prevents or limits tax-exempt entities from engaging in businesses that are unrelated to their primary purposes.

When must an organization pay UBIT?

An exempt organization that has $1,000 or more of gross income from an unrelated business must file Form 990-T PDF. An organization must pay estimated tax if it expects its tax for the year to be $500 or more.

What rate is Ubti taxed at?

37%

Thanks to President Trump, the 2019 Unrelated Business Income Tax (UBTI or UBIT) rate is 37%. This is the same as 2018. The UBTI tax is not a widely known tax because it generally only applies to tax-exempt organizations. This includes charities and retirement accounts.

How do you avoid Ubti?

How Tax-Exempt Investors Can Avoid UBTI: Structuring Private Equity Investments in LLCs

- Electing Out of Investments.

- Use of Debt or Options.

- Use of Blockers and Feeders.

- Conclusion.

What do you need to know about UBTI deductions?

To qualify as allowable deductions in computing UBTI, the expenses, depreciation, and similar items generally must be allowable income tax deductions that are directly connected with car- rying on the unrelated trade or business to which they relate. They can’t be directly con- nected with excluded income.

Do you have to calculate UBTI for unrelated business?

Separate UBTI calculation for each trade or business. Organizations with more than one unrelated trade or business must compute unrelated business taxable income (UBTI), including for purposes of determining any net operating loss deduction, separately with respect to each trade or business. See Schedule M (Form 990-T).

What is unrelated business taxable income in Wisconsin?

The unrelated business taxable income subject to Wisconsin tax is the amount computed under Section 512, Internal Revenue Code.

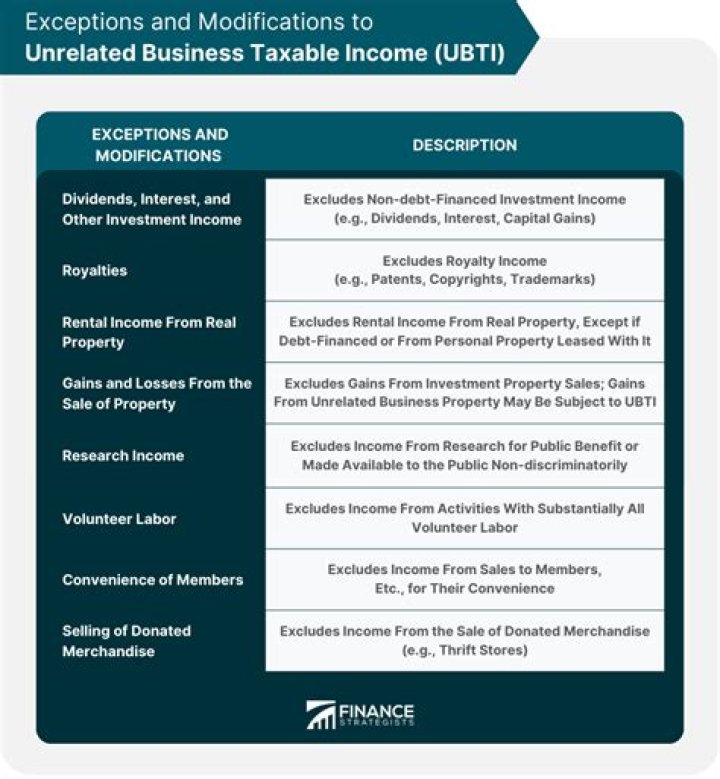

What are the exceptions to UBTI and UBIT?

The UBTI and UBIT determinations vary on a case-by-case basis because of many exceptions, exclusion and modifications to the law, many of which do not make much sense. Passive income, such as dividend and interest income, royalties and rents from real estate property