What is a make-or-buy analysis?

Robert Harper

Robert Harper

March 11, 2021. The make or buy decision involves whether to manufacture a product in-house or to purchase it from a third party. The outcome of this analysis should be a decision that maximizes the long-term financial outcome for a company.

What makes or buy decisions are involved?

What Is a Make-or-Buy Decision? Also referred to as an outsourcing decision, a make-or-buy decision compares the costs and benefits associated with producing a necessary good or service internally to the costs and benefits involved in hiring an outside supplier for the resources in question.

When performing a make buy analysis what buy cost must be included when comparing the two costs?

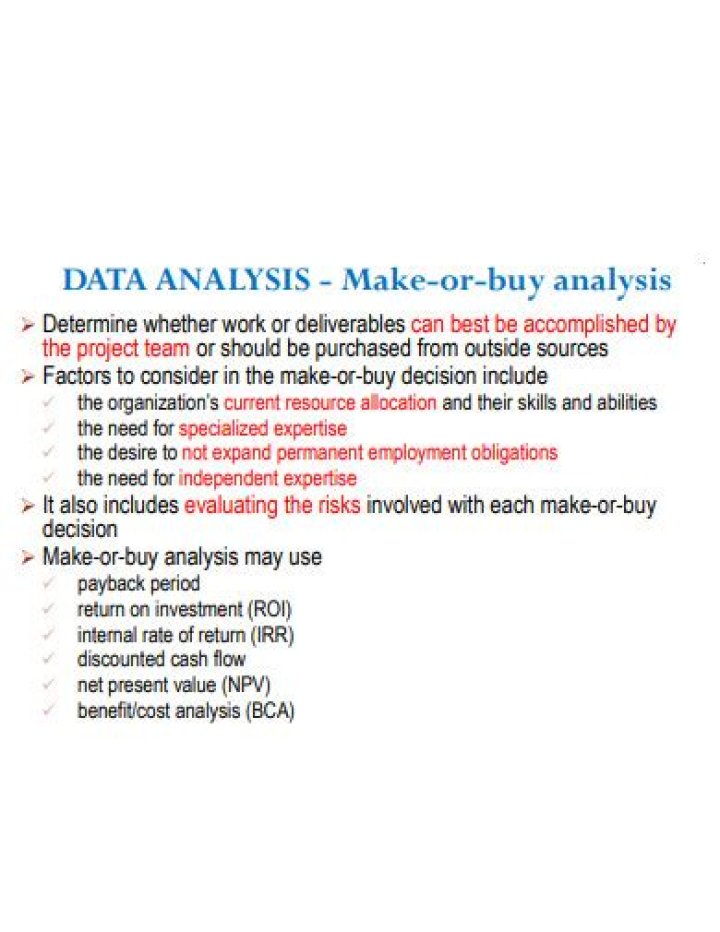

When performing a make/buy analysis, what “buy” cost must be included when comparing the two costs? Answer: B – Fixed overhead must be included in cost calculations when making or buying a product or service. Fixed overhead is a cost incurred whether buying or making.

During which procurement process is make-or-buy analysis performed?

The very first tool & technique of the process 12.1 Plan Procurement Management is the Make-or-Buy Analysis. If the decision is made to do all the project work in-house, as opposed to purchasing some components of the project work from outside sources, then there will be no procurements.

What are the benefits of a make or buy analysis?

One of the most notable advantages that a company enjoys when embracing a make-or-buy decision approach is that it can lower costs and increase capital investments, regardless of whether it decides to make materials in-house or subcontract from an external vendor.

Why is make-or-buy analysis important?

The make-or-buy decision is important in project management as it helps project managers decision where to source their task.

What is meant by value analysis?

Value analysis is an approach to improving the value of a product or process by understanding its constituent components and their associated costs. It then seeks to find improvements to the components by either reducing their cost or increasing the value of the functions.

How do you calculate special order decisions?

Calculate the contribution margin (price – variable costs) per unit for the special order. Exclude irrelevant costs from the calculation. Multiply the number of units in the special order by the contribution margin per unit. If there are any incremental fixed costs, subtract those costs from the contribution margin.

What is an example of value analysis?

Value Analysis: Examples A product manager at a company that produced nails had received several requests from customers for a nail that could not work loose. Identifying this ‘improved nail’ as a possible new product line, he decided to do a Value Analysis to help identify costs and values.

How do you conduct value analysis?

Value Analysis: How to do it

- Identify and prioritize the customers of the item from step 1.

- Identify the basic functions of the item or process from step 1.

- Identify the secondary functions of the item by finding other functions that support the basic functions from step 2.

What is the formula for calculating cost-benefit analysis?

The formula for benefit-cost ratio is: Benefit-Cost Ratio = ∑ Present Value of Future Benefits / ∑ Present Value of Future Costs.