What is an opening balance sheet in accounting?

David Craig

David Craig

An opening balance sheet contains the beginning balances at the start of a reporting period. If a business has just begun, then the opening balance sheet will contain no account balances at all, or perhaps the equity contributions (and offsetting cash balances) of investors.

Do accountants look at balance sheets?

You and your accountant can identify the liabilities on balance sheets by looking for the word “payable.” Again, these liabilities are some of the sources of your company’s assets.

How do you calculate balance sheet in accounting?

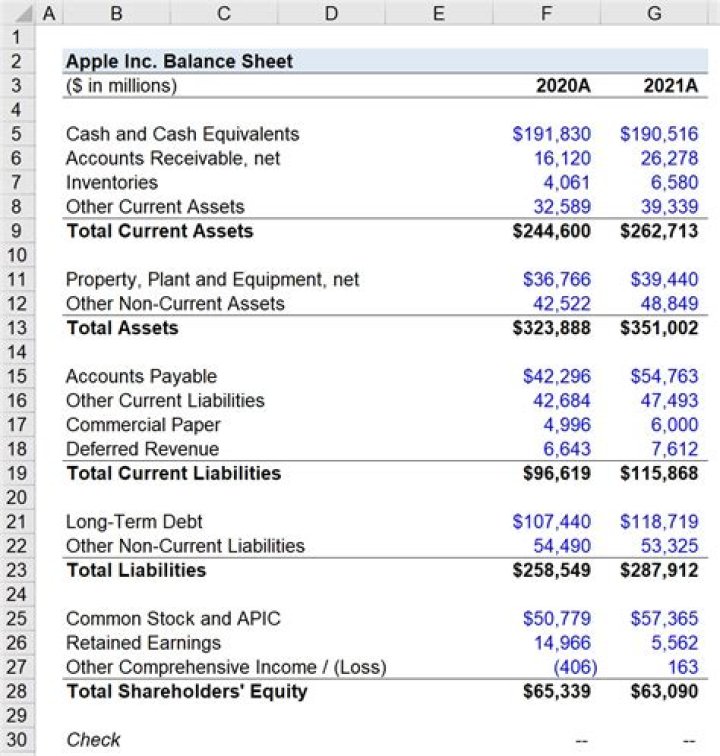

The balance sheet is based on the fundamental equation: Assets = Liabilities + Equity. As such, the balance sheet is divided into two sides (or sections).

Why does a balance sheet balance?

The major reason that a balance sheet balances is the accounting principle of double entry. This accounting system records all transactions in at least two different accounts, and therefore also acts as a check to make sure the entries are consistent.

Why do balance sheets have to balance?

Why do we prepare projected balance sheet?

A projected balance sheet is also referred to as a pro forma balance sheet. It shows the estimation of the total assets and total liabilities of any business. A pro forma balance sheet is a tabulation of future projections. As a result, it will help your business manage your assets now for better results in the future.

What are liabilities on a balance sheet?

A liability is something a person or company owes, usually a sum of money. Recorded on the right side of the balance sheet, liabilities include loans, accounts payable, mortgages, deferred revenues, bonds, warranties, and accrued expenses.

How do you fix balance sheet balance?

Answer 1: “Plug” the balance sheet (i.e. enter hardcodes across one row of the Balance Sheet for each year that doesn’t balance). Answer 2: Wire the balance sheet so that it always balances by making Retained Earnings equal to Total Assets less Total Liabilities less all other equity accounts.

What have you learned in giving steps in managing your own financial expenses?

Understand your income. Consolidate your debt. Slash or remove unnecessary expenses. Review and understand your credit report.