What is income reconciliation?

Nathan Sanders

Nathan Sanders

Revenue reconciliation is the act of reconciling all sales (services provided or goods delivered) and cash received in a specific period to determine what should be recorded on the Income Statement (P&L) and Balance Sheet.

How do you reconcile an income statement?

Take the appropriate figures from the income statement and add them to your reconciliation. Start your reconciliation with net income at the top. Add back the total value of noncash expenses to your operating cash flow. Next, subtract the period change for each category of current assets.

How do you reconcile in accounting?

Once you’ve received it, follow these steps to reconcile a bank statement:

- COMPARE THE DEPOSITS. Match the deposits in the business records with those in the bank statement.

- ADJUST THE BANK STATEMENTS. Adjust the balance on the bank statements to the corrected balance.

- ADJUST THE CASH ACCOUNT.

- COMPARE THE BALANCES.

How do you reconcile income from taxable income?

Tax Return Reconciliation The schedules start with accounting income, increase it with expenses that aren’t tax-deductible and income that is taxable but not yet reported on the books, then decreases it for book income that’s not taxed and tax deductions that exceed book expenses.

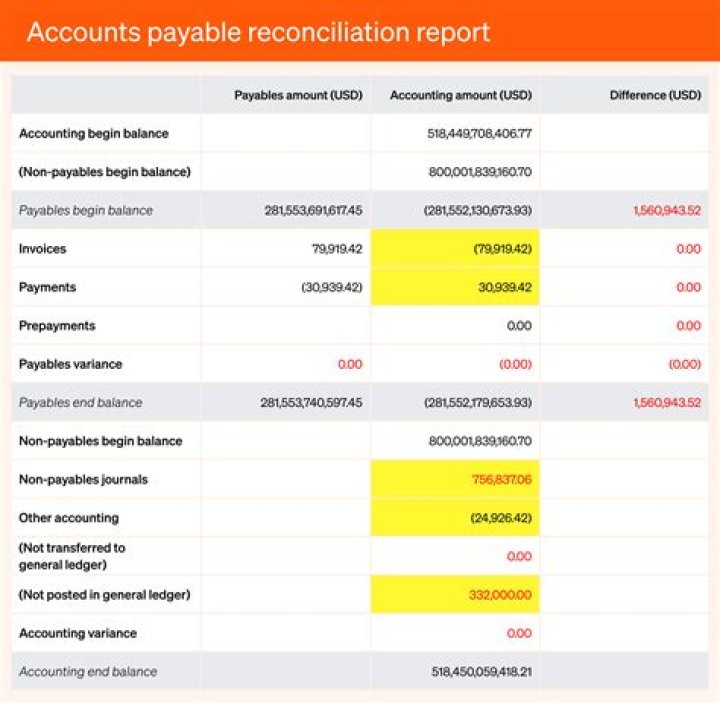

Why do we do balance sheet reconciliation?

Balance sheet reconciliation verifies the accuracy of the balance sheet by comparing the numbers on the general ledger to other forms of documentation, to explain any discrepancies. Essentially, reconciliation is done to verify that accounting for a certain period has been accurately portrayed on a company’s books.

Is book income the same as net income?

Certain differences in book and tax income will never be reversed. Some common permanent differences include: For tax purposes, a company can only deduct 50%of meals and 0% of entertainment expenses. Municipal bond interest – This is considered net income for book accounting, but it is not included in taxable income.

What is an M adjustment?

M-1 adjustments: reconciliation of book and taxable income (income and deductions.) These deferred tax assets and deferred tax liabilities develop due to timing differences of income and deductions for book and tax purposes.

What are the 5 steps to checkbook reconciliation?

How to Balance a Checkbook: Step-by-Step

- Step 1: Recording your transactions.

- Step 2: Review your monthly bank statement.

- Step 3: Check that your balances match.

- Step 4: Address any errors or fraudulent activity.

- Step 5: Draw a line in your register.

- Step 6: File your bank statement.

What is P&L reconciliation?

There are two primary profit and loss (P&L) reconciliations performed by product control. These are the comparison of the front office estimate to product control’s P&L and the comparison of the P&L in the general ledger (GL) to that reported by product control.

What are reconciliation entries?

Reconciliation allows an importer to revise certain elements of an entry summary that were undeterminable at the time the merchandise was entered, such as, value, 9802, classification, and FTA. As an entry, a Reconciliation may be liquidated, rejected, or change liquidated.