What is section 174 expenses?

Nathan Sanders

Nathan Sanders

Section 174 requires that R&E expenses be incurred “in connection with a trade or business” in order to be currently deductible. All that is required is that there be a “realistic prospect” that the inventor’s efforts will result in a trade or business at some time.

What is sec 174?

Section 174 of the Code of Criminal Procedure is a legal provision that deals with the procedure that the police and the magistrate need to follow in cases of suicide and unnatural death. When a person does not die due to the natural circumstances, a person is considered victim of unnatural death.

What qualified research expenses?

QUALIFIED RESEARCH EXPENSES (“QREs”) any “wages” paid or incurred to an employee for “qualified services” performed by such employee; under regulations prescribed by the Secretary, any amount paid or incurred to another person for the right to use computers in the conduct of qualified research.

What costs qualify for r& d credit?

Certain costs incurred during the development or improvement of products, processes, techniques, formulas, inventions or software that meet specific IRS requirements are considered qualified research expenses1. Examples include employee wages, contract research expenses and supply costs.

What CrPC 172?

Under the provision of Section 172 of the Criminal Procedure Code (CrPC) a police officer conducting the investigation is required to maintain a record of investigation done on each day in a particular case. A case diary is important to record the investigation carried out by an Investigating Officer.

What is Section 173 of the Cr PC?

Sub-section (1) of Section 173 of CrPC provides that every investigation by the police shall be completed without unnecessary delay and sub-section (2) of Section 173 CrPC provides that as soon as such investigation is completed, the officer in charge of the police station shall forward to a Magistrate empowered to …

Can you write off research expenses?

As an incentive to engage in research and development, the IRS permits businesses to deduct all R&D expenses in a single year instead of amortizing as a capital expense. However, you must generally decide to deduct R&D expenditures as a regular expense in the first year you incur expenses.

Why was section 174 created by the IRS?

IRS Clarifies Section 174 Regulations. Section 174 was enacted to encourage taxpayers to conduct research activities by providing certainty about the deductibility of their research expenses. In general, unless a taxpayer elects to defer and amortize its research expenses, Section 174 provides that a taxpayer is entitled to deduct,…

How does section 174 affect research and development?

The modifications made to Section 174 include a new subsection that specifically includes any amount paid or incurred in connection with software development as a research or experimental expenditure (and, therefore, within the scope of the provision). Presently, these costs may be deducted or amortized under Revenue Procedure 2000-50.

What kind of expenses can you deduct under Section 174?

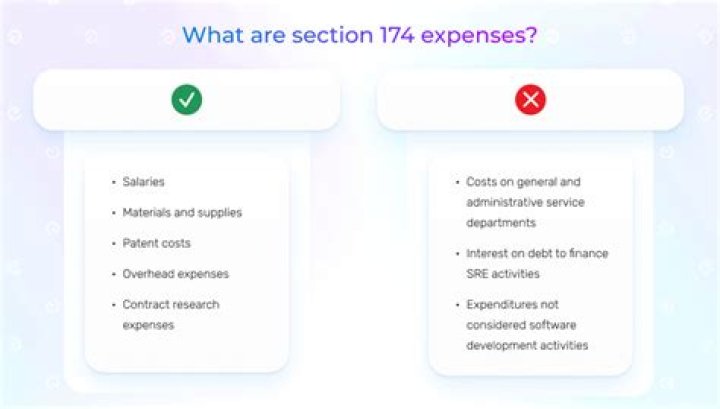

Only expenses for research and experimentation (“R&E”) are deductible under Section 174. What exactly is R&E?

When do you amortize QRES under IRC Section 174?

IRC Section 174(b) allows companies to capitalize QREs and amortize them over a period of 5 years, beginning with the month when a company first realizes benefits from an R&D investment.