What is simple moving average forecasting?

Joseph Russell

Joseph Russell

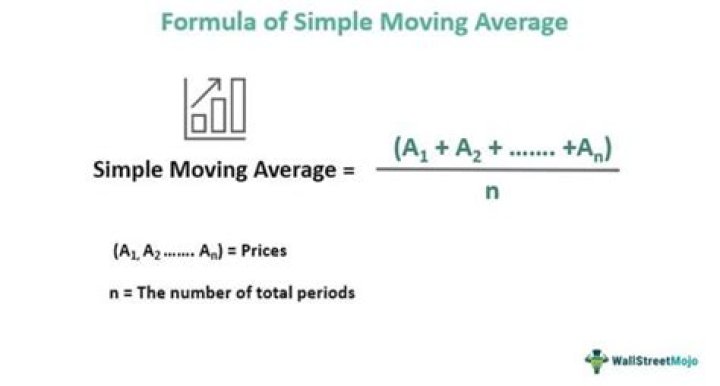

A simple moving average (SMA) calculates the average of a selected range of prices, usually closing prices, by the number of periods in that range. A simple moving average is a technical indicator that can aid in determining if an asset price will continue or if it will reverse a bull or bear trend.

What is moving average time series model?

Moving averages are a simple and common type of smoothing used in time series analysis and time series forecasting. Calculating a moving average involves creating a new series where the values are comprised of the average of raw observations in the original time series.

What is weighted moving average time series forecasting?

A Weighted Moving Average puts more weight on recent data and less on past data. This is done by multiplying each bar’s price by a weighting factor. Because of its unique calculation, WMA will follow prices more closely than a corresponding Simple Moving Average.

What are the types of moving average?

There are four different types of moving averages: Simple (also referred to as Arithmetic), Exponential, Smoothed and Weighted. Moving Average may be calculated for any sequential data set, including opening and closing prices, highest and lowest prices, trading volume or any other indicators.

What is an AR 2 model?

An AR(1) autoregressive process is one in which the current value is based on the immediately preceding value, while an AR(2) process is one in which the current value is based on the previous two values. An AR(0) process is used for white noise and has no dependence between the terms.

What is least square method in time series?

Least Square is the method for finding the best fit of a set of data points. It minimizes the sum of the residuals of points from the plotted curve. It gives the trend line of best fit to a time series data. This method is most widely used in time series analysis.

Is an AR 2 process stationary?

This is a non-stationary explosive process. If we combine all the inequalities we obtain a region bounded by the lines φ2 =1+ φ1; φ2 = 1 − φ1; φ2 = −1. This is the region where the AR(2) process is stationary.

What is an AR 4 model?

In an autoregression model, we forecast the variable of interest using a linear combination of past values of the variable. The term autoregression indicates that it is a regression of the variable against itself. We refer to this as an AR(p ) model, an autoregressive model of order p .

What is least square method formula?

Least Square Method Formula

- Suppose when we have to determine the equation of line of best fit for the given data, then we first use the following formula.

- The equation of least square line is given by Y = a + bX.

- Normal equation for ‘a’:

- ∑Y = na + b∑X.

- Normal equation for ‘b’:

- ∑XY = a∑X + b∑X2

What is least square moving average?

The least square moving average (LSMA) calculates the least squares regression line for the preceding time periods, thus leading to forward projections from the current period. Accordingly, the indicator has the ability to identify what could happen if the regression line continued.

Are autoregressive models stationary?

Contrary to the moving-average (MA) model, the autoregressive model is not always stationary as it may contain a unit root.

Is an AR 1 process stationary?

The AR(1) process is stationary if only if |φ| < 1 or −1 <φ< 1. This is a non-stationary explosive process. If we combine all the inequalities we obtain a region bounded by the lines φ2 =1+ φ1; φ2 = 1 − φ1; φ2 = −1. For the stationarity condition of the MA(q) process, we need to rely on the general linear process.

How do AR models forecast?

Forecasting with AutoRegressive (AR) Model in R

- Step 1: Fit the model. The first step is to fit the model as ARIMA(1, 0, 0) .

- Step 2: Create Forecast. We can now use the predict() function to create a forecast using the fitted AR model.

- Step 3: Plot the Forecast.

- Step 4: Add Confidence Intervals to Forecast.

What is the least square criterion?

The least squares criterion is a formula used to measure the accuracy of a straight line in depicting the data that was used to generate it. That is, the formula determines the line of best fit. This mathematical formula is used to predict the behavior of the dependent variables.