What is the cost principle in financial reporting?

Sophia Bowman

Sophia Bowman

The cost principle is an accounting principle that requires assets, liabilities, and equity investments to be recorded on financial records at their original cost. The cost principle is also known as the historical cost principle and the historical cost concept.

What is the basis of preparing financial statement?

The financial statements have been prepared on an accrual basis and in accordance with the historical cost convention, except for certain assets and liabilities at fair value. Except where stated, no allowance is made for the effect of changing prices on the results or the financial position.

How cost principle is applied in a company financial statement?

Generally, the cost principle requires that only the verifiable, historical costs recorded at the time of transactions will appear as expenses on the income statement. Unfortunately those recorded costs may not measure the economic reality that is occurring in the period of the income statement.

What principles are involved in preparing the different financial statements?

According to IAS 1 general features of financial statements (which can also be called as fundamental principles for preparation and presentation of financial statements) are:

- Fair presentation and compliance with IFRSs.

- Going concern.

- Accrual basis of accounting.

- Materiality and aggregation.

- Offsetting.

- Reporting annually.

What are the basic financial statement?

There are four main financial statements. They are: (1) balance sheets; (2) income statements; (3) cash flow statements; and (4) statements of shareholders’ equity. Balance sheets show what a company owns and what it owes at a fixed point in time.

What is basis of preparation?

In preparing these consolidated financial statements, management has made judgements and estimates that affect the application of the Group’s accounting policies and the reported amounts of assets, equity, liabilities, commitments, income and expenses.

What are disadvantages of cost principle?

Lack of accuracy The cost principle can only take into account the initial value of an asset at the time a company acquires it. The cost principle may not take into account any increases in market value to the assets, nor can it report on the depreciation of the asset over time.

What is basis of presentation?

Basis of presentation describes the underlying basis used to prepare the financial statements (for example, US Generally Accepted Accounting Principles, Other Comprehensive Basis of Accounting, IFRS). Accounting policies describe all significant accounting policies of the reporting entity.

Which GAAP principle is applicable?

Principle of Regularity: GAAP-compliant accountants strictly adhere to established rules and regulations. Principle of Consistency: Consistent standards are applied throughout the financial reporting process. Principle of Sincerity: GAAP-compliant accountants are committed to accuracy and impartiality.

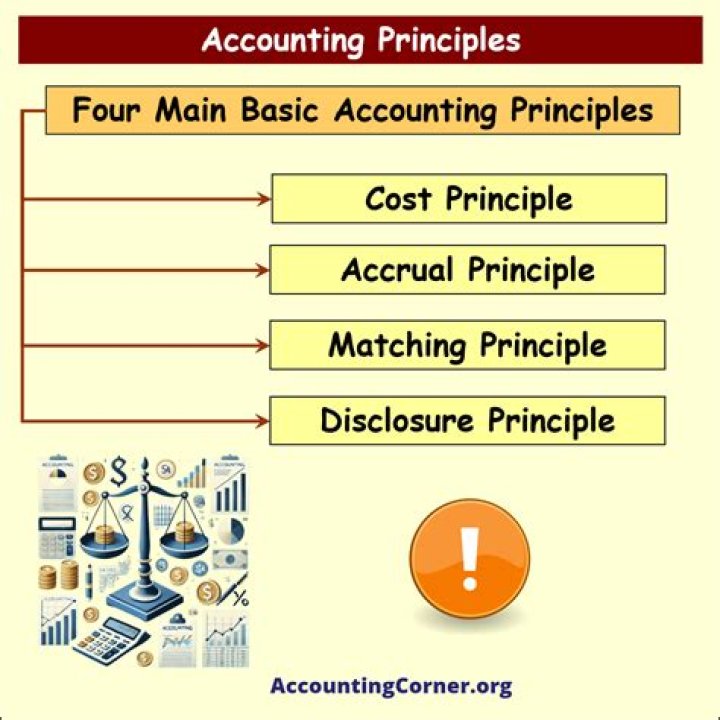

Generally accepted accounting principles (GAAP) is the name of the rules and regulations used to prepare financial statements….5 principles of accounting are;

- Revenue Recognition Principle,

- Historical Cost Principle,

- Matching Principle,

- Full Disclosure Principle, and.

- Objectivity Principle.

Which method is not commonly used as it Cannot help in the preparation of financial statements?

Totals Method

1] Totals Method However, totals method is not in use widely as it does not determines the accurate balances of the accounts and thus, also does not help in the preparation of the Financial statements or final accounts.

What are the principles of accrual basis accounting?

A. Recognition principle. B. Cost principle. C. Cash basis of accounting. D. Matching principle. E. Time period principle. c The system of preparing financial statements based on recognizing revenues when the cash is received and reporting expenses when the cash is paid is called: A. Accrual basis accounting.

What is the principle of the cost benefit principle?

Cost Benefit Principle – limits the required amount of research and time to record or report financial information if the cost outweighs the benefit. Thus, if recording an immaterial event would cost the company a material amount of money, it should be forgone.

Do you know the basic principles of accounting?

It’s important to have a basic understanding of these main accounting principles as you learn accounting. This isn’t just memorizing some accounting information for a test and then forgetting it two days later. These principles show up all over the place in the study of accounting.

What is the going concern principle in accounting?

Going concern principle: A business will continue to exist and function with no defined end date. Matching principle: Businesses should use the accrual basis of accounting and report all financial information using this method. Revenue recognition principle: Revenue is reported when it’s earned, regardless of when payment is actually received.