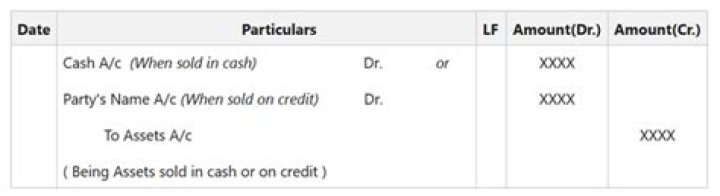

What is the entry for sale of asset?

David Craig

David Craig

Debit cash for the amount received, debit all accumulated depreciation, debit the loss on sale of asset account, and credit the fixed asset. Gain on sale. Debit cash for the amount received, debit all accumulated depreciation, credit the fixed asset, and credit the gain on sale of asset account.

How do you calculate net book value of an asset?

Net book value, also known as net asset value, is the value at which a company reports an asset on its balance sheet. It is calculated as the original cost of an asset less accumulated depreciation, accumulated amortization, accumulated depletion or accumulated impairment.

How do you calculate asset sales?

The original purchase price of the asset, minus all accumulated depreciation and any accumulated impairment charges, is the carrying amount of the asset. Subtract this carrying amount from the sale price of the asset. If the remainder is positive, it is a gain.

How do you calculate the initial cost of an asset?

The original cost of an asset encompasses more than the asset’s purchase price, and the costs added together can reduce the potential taxable gain on the sale of the asset. The tax basis can be calculated by taking the original cost and subtracting the accumulated depreciation of the asset.

What is the journal entry for the sale of an asset at book value?

At the time of disposal, depreciation expense should be recorded to update the asset’s book value. A journal entry is recorded to increase (debit) depreciation expense and increase (credit) accumulated depreciation. Depreciation expense is reported on the income statement as a reduction to income.

Is gain on sale a revenue?

When your company sells off an asset or investment, any gain on the sale should be reported on your income statement, the financial statement that tracks the flow of money into and out of your business. However, because of the circumstances under which you received this money, the gain should not be counted as revenue.

When an asset is no longer useful but Cannot be sold?

When a long-term asset is no longer useful but cannot be sold, we have a retirementFor example, we physically remove a baking oven that no longer works and also remove it from the accounting records through a retirement entry. C. An exchangeoccurs when two companies trade assets.

How do you you recognize the revenue and gains?

According to the principle, revenues are recognized when they are realized or realizable, and are earned (usually when goods are transferred or services rendered), no matter when cash is received. In cash accounting – in contrast – revenues are recognized when cash is received no matter when goods or services are sold.

Is selling assets debit or credit?

Sales revenue is posted as a credit. Increases in revenue accounts are recorded as credits as indicated in Table 1. Cash, an asset account, is debited for the same amount. An asset account is debited when there is an increase.

What is the normal balance entry of an asset?

Asset accounts normally have debit balances, while liabilities and capital normally have credit balances. Income has a normal credit balance since it increases capital . On the other hand, expenses and withdrawals decrease capital, hence they normally have debit balances.

How do you account for the sale of a fully depreciated asset?

Fully depreciated asset: With zero proceeds from the disposal, debit accumulated depreciation and credit the fixed asset account. Gain on asset sale: Debit cash for the amount received, debit all accumulated depreciation, credit the fixed asset, and credit the gain on sale of the asset account.

Do you debit or credit the sale of an asset?

Debit cash for the amount received, debit all accumulated depreciation, credit the fixed asset, and credit the gain on sale of asset account.

How to record the sale of an asset?

No proceeds, fully depreciated. Debit all accumulated depreciation and credit the fixed asset. Loss on sale. Debit cash for the amount received, debit all accumulated depreciation, debit the loss on sale of asset account, and credit the fixed asset. Gain on sale.

How are the entries defined when selling a fixed asset?

Defining the Entries When Selling a Fixed Asset. When a fixed asset or plant asset is sold, there are several things that must take place: The fixed asset’s depreciation expense must be recorded up to the date of the sale. The fixed asset’s cost and the updated accumulated depreciation must be removed. The cash received must be recorded.

How much does a sales journal entry debit?

The customer charges a total of $252 on credit ($240 + $12). Your credit sales journal entry should debit your Accounts Receivable account, which is the amount the customer has charged to their credit. And, you will credit your Sales Tax Payable and Revenue accounts.