What is the interest and penalties for a IRS late payment?

Isabella Wilson

Isabella Wilson

Failure-to-pay penalty is charged for failing to pay your tax by the due date. The late payment penalty is 0.5% of the tax owed after the due date, for each month or part of a month the tax remains unpaid, up to 25%. You won’t have to pay the penalty if you can show reasonable cause for the failure to pay on time.

Does interest accrue on IRS penalties?

When processing is complete, if you owe any tax, penalty, or interest, you will receive a bill. Generally, interest accrues on any unpaid tax from the due date of the return until the date of payment in full. The interest rate is determined quarterly and is the federal short-term rate plus 3 percent.

When to pay penalties and interest on taxes?

To keep interest and penalties to a minimum, taxpayers should file their tax return and pay any tax owed as soon as possible. Here are some facts that taxpayers should know:

What’s the penalty for not filing taxes by the due date?

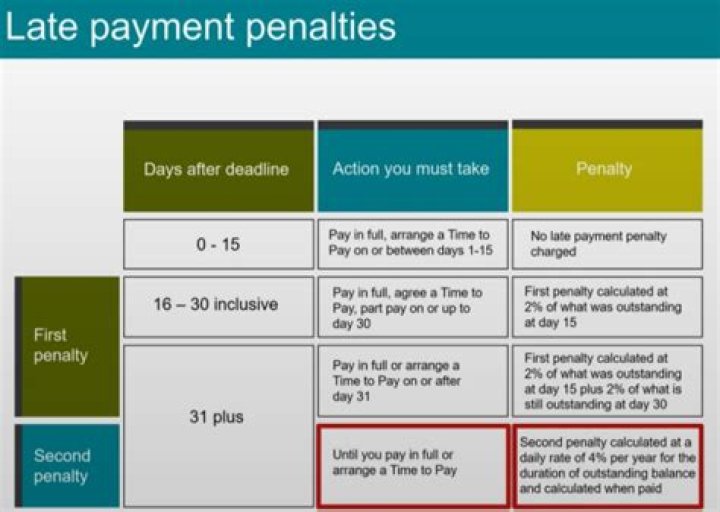

If taxpayers file their 2016 tax return more than 60 days after the due date or extended due date, the minimum penalty is $205 or, if they owe less than $205, 100 percent of the unpaid tax. Otherwise, the penalty can be as much as 5 percent of their unpaid taxes each month up to a maximum of 25 percent.

What should I do if I owe a penalty to the IRS?

If applicable, the report from the IRS listing the penalty that relates to the incorrect advice. Generally, you should file a Form 843, Claim for Refund and Request for Abatement, to request penalty relief based on incorrect written advice from the IRS. What if the IRS denies my penalty abatement request?

Is there a limit to the amount of interest the IRS can charge on late taxes?

There is no maximum limit to the failure-to-pay penalty. The IRS will charge interest on late or unpaid taxes, regardless of cause. The period covered always begins with the original due date of the return, and ends with the receipt of payment by the IRS.