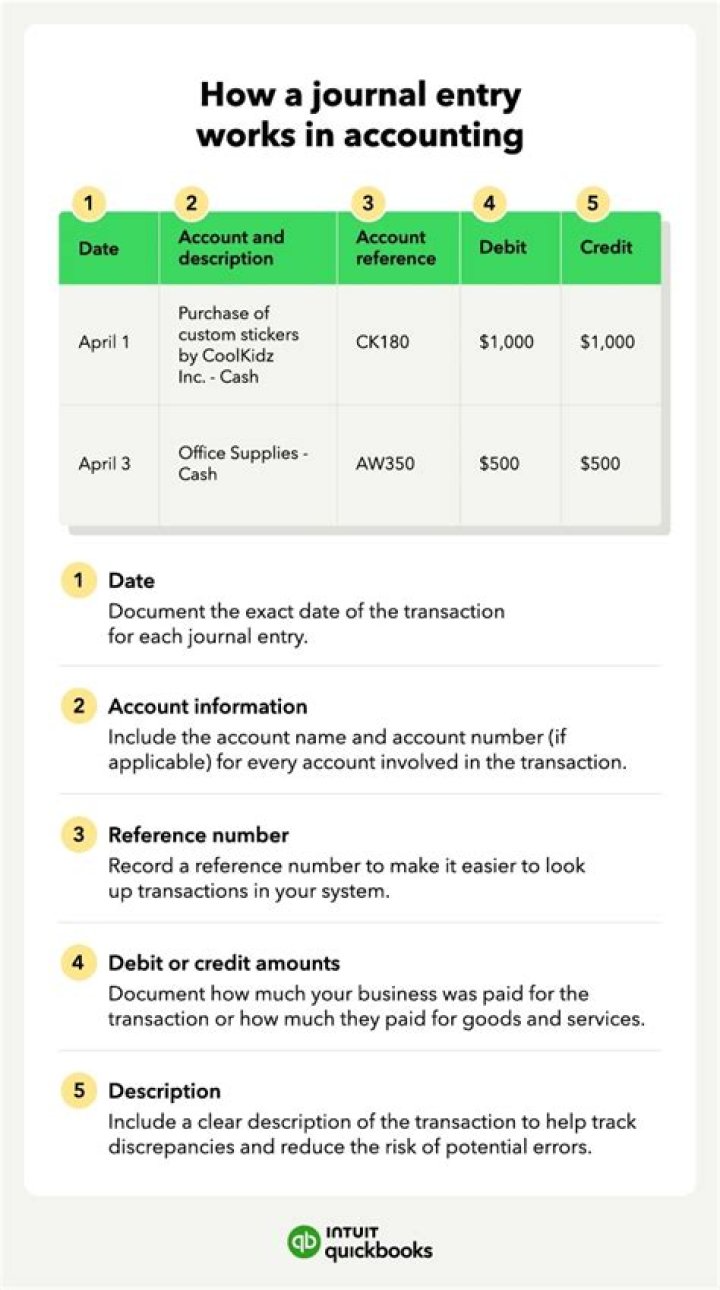

What is the journal entry to close a revenue?

Robert Harper

Robert Harper

Closing the revenue accounts—transferring the credit balances in the revenue accounts to a clearing account called Income Summary. Closing the expense accounts—transferring the debit balances in the expense accounts to a clearing account called Income Summary.

How do you Journalize closing entries?

Four Steps in Preparing Closing Entries

- Close all income accounts to Income Summary.

- Close all expense accounts to Income Summary.

- Close Income Summary to the appropriate capital account. Owner’s capital account for sole proprietorship.

- Close withdrawals/distributions to the appropriate capital account.

Do closing entries affect revenue?

If a company’s revenues are greater than its expenses, the closing entry entails debiting income summary and crediting retained earnings.

Why are closing entries made?

Closing entries take place at the end of an accounting cycle as a set of journal entries. The closing entries serve to transfer the balances out of certain temporary accounts and into permanent ones. This resets the balance of the temporary accounts to zero, ready to begin the next accounting period.

How do you account for revenue?

The accrual journal entry to record the sale involves a debit to the accounts receivable account and a credit to sales revenue; if the sale is for cash, debit cash instead. The revenue earned will be reported as part of sales revenue in the income statement for the current accounting period.

This is done through a journal entry debiting all revenue accounts and crediting income summary. Next, the same process is performed for expenses. All expenses are closed out by crediting the expense accounts and debiting income summary. Third, the income summary account is closed and credited to retained earnings.

What are post closing journal entries?

Post closing entries are the only entries that will adjust the prior year balances on the balance sheet accounts. General journal entries will not adjust the prior year balances. In order to process any post closing entries, the Allow Prior Period Transactions option will have to be enabled.

The first two entries: Closing out Revenues and Expenses We will close out the revenues by getting rid of the current balances. In other words, revenues have credit balances, so we will debit them to wipe them out. The offsetting entry will go to Income Summary.

How do you close entries in accounting?

Does QuickBooks automatically make closing entries?

QuickBooks Desktop doesn’t have an actual transaction for closing entries it automatically creates. The program computes the adjustments when you run a report (for example QuickReport of Retained Earnings) but you can’t “QuickZoom” on these transactions, unlike the manual adjustments you recorded.

What happens to service revenue after closing entries?

After preparing the closing entries above, Service Revenue will now be zero. The expense accounts and withdrawal account will now also be zero.

Where do closing entries journals go in accounting?

All these examples of closing entries journals have been debited in the expense account. Now at the end of the accounting year 2018, the expense account needs to be credited to clear its balances, and the Income summary account should be debited.

Where do closing entries go in the general ledger?

So for posting the closing entries in the general ledger, the balances from revenue and expense account will be moved to the income summary account. Income summary account is also a temporary account that is just used at the end of the accounting period to pass the closing entries journal.

How are revenue accounts and expense accounts closed?