What items appear on the book side of a bank reconciliation?

Emma Jordan

Emma Jordan

The following reconciling items commonly arise as part of a bank reconciliation, and require adjustment of the book balance:

- Interest earned. This amount is recorded in the bank statement, and must be added to the company’s book balance.

- Service charges.

- Adjustments to deposits.

- Adjustments to checks.

What is bank side and book side?

Book Ledger. The “bank side,” or bank ledger, simply refers to whatever record of bank transactions is used to reconcile accounts with a company’s book ledger.

Which one of the following items is a reconciling item on the bank side of a bank reconciliation?

The correct answer is c. deposit in transit and outstanding checks. While reconciling the bank balance, we add deposit in transit and subtract…

Do unrecorded deposits affect the bank side or checkbook side?

Unrecorded deposits affect the checkbook side.

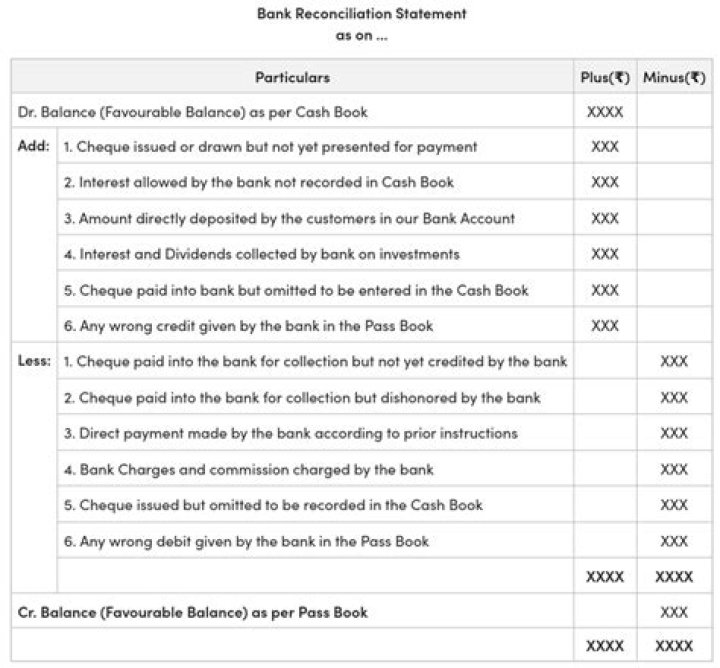

How do I prepare a bank reconciliation?

Here are the steps for completing a bank reconciliation:

- Get bank records.

- Gather your business records.

- Find a place to start.

- Go over your bank deposits and withdrawals.

- Check the income and expenses in your books.

- Adjust the bank statements.

- Adjust the cash balance.

- Compare the end balances.

What is true of a bank reconciliation?

A bank reconciliation is the process of matching the balances in an entity’s accounting records for a cash account to the corresponding information on a bank statement. The goal of this process is to ascertain the differences between the two, and to book changes to the accounting records as appropriate.

How do you prepare a reconciliation?

Steps in Preparation of Bank Reconciliation Statement

- Check for Uncleared Dues.

- Compare Debit and Credit Sides.

- Check for Missed Entries.

- Correct them.

- Revise the Entries.

- Make BRS Accordingly.

- Add Un-presented Cheques and Deduct Un-credited Cheques.

- Make Final Changes.

Do all items on the book side of the bank reconciliation require journal entries?

The items on the bank reconciliation that require a journal entry are the items noted as adjustments to books. These are the items that appear on the bank statement, but are not yet recorded in the company’s general ledger accounts.

Book Ledger. The “bank side,” or bank ledger, simply refers to whatever record of bank transactions is used to reconcile accounts with a company’s book ledger. More often than not, this will be a monthly bank statement.