What to do if you receive a 1099-C?

Robert Harper

Robert Harper

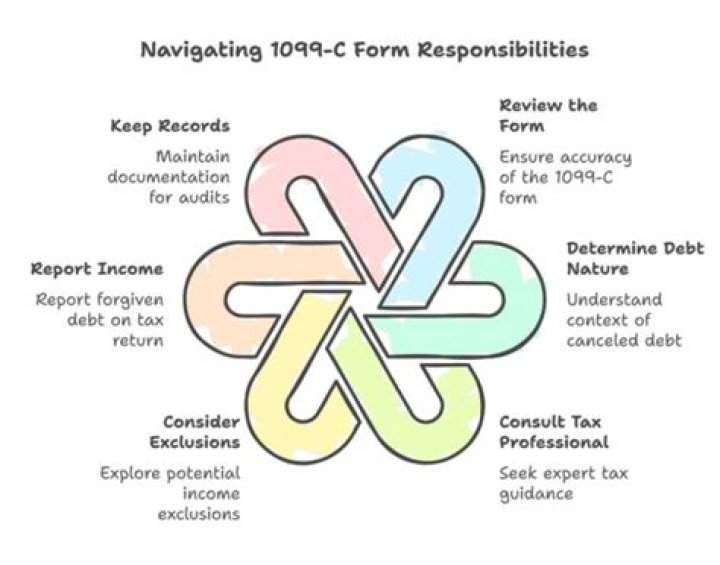

If you receive a 1099-C for a debt you were not aware was discharged, clarify the status of the debt with the creditor. If they are following the old rule, request that they rescind the 1099-C under Internal Revenue Bulletin 2016-48, T.D. 9793. Rescinding the 1099-C will alert the IRS that it was issued in error.

When do creditors no longer need to issue a 1099-C?

Under an IRS rule change effective in November 2016, creditors are no longer expected to issue a 1099-C form merely because debt has gone 36 months without a payment. If you receive a 1099-C for a debt you were not aware was discharged, clarify the status of the debt with the creditor.

What kind of debt is excluded on a 1099-C?

First, find out whether the type of debt cancellation on the 1099-C form is excluded from taxable income. The IRS provides a list of exclusions, which include debts that were forgiven because you were insolvent or involved in certain types of bankruptcies.

Do you get a 1099 when you cancel a credit card?

Months after resolving credit card debts, consumers may receive 1099-C “Cancellation of Debt” tax notices in the mail. Here’s why Many consumers aren’t aware that forgiven credit card debt may be taxable income, and it shows up on an IRS 1099-C form

Why is the IRS no longer issuing 1099-C forms?

The IRS Taxpayer Advocate Service cited the resulting confusion in its annual reports to Congress as a priority for the agency to clear up. Under an IRS rule change effective in November 2016, creditors are no longer expected to issue a 1099-C form merely because debt has gone 36 months without a payment.

What does the right side of Form 1099-C show?

The right side of the form has seven boxes: Box 1: Date of identifiable event. Box 1 shows the date the earliest identifiable event occurred or the date of when the debt was discharged. Box 2: Amount of debt discharged.

What does Form 1099-C cancellation of debt mean?

What Is Form 1099-C: Cancellation of Debt? Form 1099-C (entitled Cancellation of Debt) is one of a series of “1099” forms used by the Internal Revenue Service (IRS) to report various payments and transactions, excluding employee wages.

What’s the difference between Form 1099 a and 1099 C?

1099-A and Form 1099-C, Cancellation of Debt, for the same debtor. You may file Form 1099-C only. You will meet your Form 1099-A filing requirement for the debtor by completing boxes 4, 5, and 7 on Form 1099-C. However, if you file both Forms 1099-A and 1099-C, do not complete boxes 4, 5, and 7 on Form 1099-C. See the

How much do you have to pay for a 1099 form?

Freelance and independent contractors receive these types of forms after getting at least $600 in payment. Other types require $10 as the reporting amount for things like royalties, awards, and prizes. A 1099-OID is for Original Issue Discount, the minimum amount that should be reported for this type of form is $10.

Can a 1099-C form be used for paycheck protection?

In a change for this tax filing season, the IRS told lenders not to send taxpayers 1099-C forms for the forgiveness of debt under the Paycheck Protection Program. The program often referred to as the PPP, provided forgivable loans to businesses to help them survive during the COVID-19 pandemic.

Is there Statute of limitations on filing 1099-C?

Statutes of limitations vary by state and by type of debt, but creditors are not required to file a 1099-C at that time since they can continue to try to collect on debt indefinitely.

Where to put 1099-C on a K-1?

On K-1, should I include the 1099-C amount lumped together with ordinary business income (actually loss for 2019 Ops). Or put 1099-C amount on Line 10 Other Income. 09-03-2020 10:23 PM

Why did I get a 1099-C bankruptcy form?

At its most basic level, a 1099-C reports a debt that was canceled, forgiven, never paid back or wiped out in bankruptcy. Here are some reasons you may have gotten a form 1099-C: You cut a deal with your credit card issuer and it agreed to accept less than you owed. You had a student loan or part of a student loan forgiven.

What happens if I never received a 1099c for debt?

Although, you have satisfied part one of the settlement they may not issue the 1099-C until the entire amount is satisfied. At that time the lender will report the cancellation of debt to the IRS and send you a copy of the 1099-C.

Is the schedule 1099-C a blessing or a curse?

If this happens the creditor may have no legal right to collect once the debt has been forgiven and a Schedule 1099-C issued. It’s best to discuss your personal situation with an attorney who specializes in consumer protection if you can’t resolve the issue on your own. The Form 1099-C denotes debts that have been forgiven by creditors.

What happens if you rescind a 1099-C form?

Rescinding the 1099-C will alert the IRS that it was issued in error. If the creditor will not rescind the form or confirm the debt is forgiven, you will need to use the IRS dispute process outlined in publication 4681 to show that no taxes are owed.

How does a 1099 C affect your credit?

The 1099-C form shouldn’t have any impact on your credit. However, the activity that led to the 1099-C probably does impact your credit. Typically, by the time a creditor forgives a debt, you’ve engaged in at least one of the following activities: Failed to make payments for an extended period of time

When do you need a 1099 for debt forgiveness?

Form 1099-C is a tax form required by the IRS in certain situations where your debts have been forgiven or canceled. The IRS requires a 1099-C form for certain acts of debt forgiveness because it considers that forgiven debt as a form of income. Did you find out about the negative item on your credit report?

Can a debt buyer disclose a 1099-C?

Says Maurice, the debt buyers’ attorney, “There is no current law that says that a debt buyer must disclose that a 1099-C would be forthcoming after the settlement of debt.” The Taxpayer Advocate Service has cited confusion and inadequate communication about 1099-Cs in its annual report to Congress.

When to file a 1099c discharge of indebtedness?

Filing Requirements for Form 1099C: In accordance with Internal Revenue Code (“IRC”) §6050P, discharges of indebtedness of $600 or more during any calendar year, must be reported to the Internal Revenue Service (“IRS”) on Form 1099-C.

What should I know about the insolvency exception for 1099-C?

See IRS Publication 4681 for more information about insolvency. This is a worksheet that is prepared to determine if you can qualify for eliminating taxable income form a cancelled debt (Form 1099-C). Keep it with your tax files to show proof, as well as any other documentation to substantiate it, should you need it later. 0

Do you need to complete Form 982 for 1099-C?

For each 1099-C that is not for debt forgiven for a primary residence. You need to complete an insolvency worksheet to determine your insolvency immediately prior to the forgiveness and immediately after for each case. That amount then gets entered on Form 982 for that debt discharge.

Can a 1099 C be used for a joint return?

A 1099-C is a form a debtor sends when they cancel a debt. The canceled debt is considered income. Considering your husband passed away in 2016, you cannot do a joint return this year. Therefore, there is not a return to add the income unless there was an estate opened.

How long should I wait for a 1099c?

I had cancellation of debt but did not receive a 1099c from the credit card company yet. How long should I wait? You don’t have to report anything on your tax return until you receive form 1099-C. And it depends on the lender when they will issue the form.