When a customer returns the goods a debit note is sent to him?

Robert Harper

Robert Harper

A debit note (also known as debit memo) can be issued from a buyer to their seller to indicate or request a return of funds due to incorrect or damaged goods received, purchase cancellation, or other specified circumstances.

When goods are returned by the customer he sends?

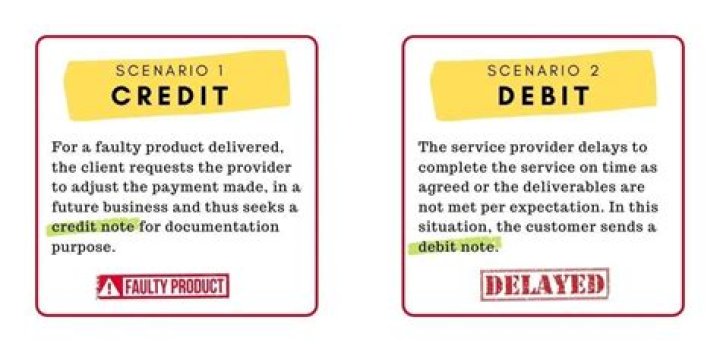

A debit note is a note which is issued when goods purchased are returned by the purchaser to the vendor or in other words when goods are returned by the buyer to the seller. A debit note signifies that the liability of the buyer has been reduced for payment or expense.

When a customer returns the goods the statement received by him from the other party is called *?

A credit note or credit memorandum is a commercial document issued by a seller to a buyer. Credit notes act as a Source document for the Sales return journal.

Is sent to the seller when he is taken back the sold goods?

A debit note is sent to the seller when he is taken back the sold goods.

When the goods are returned to a supplier?

A debit note is a commercial document issued by buyer to seller. It acts as a source document for the purchase return journal. In other words the debit note is the evidence of the reduction in purchases. It is a receipt given to supplier for return of goods to supplier, which can be offset against future transactions.

Is it sent to a customer when he returns good?

A document sent to customer when he returns the goods is called Credit note. A credit note or credit memo is a commercial document issued by a seller to a buyer.

Which is sent to the seller when he is taken back the sold goods?

debit note

A debit note is sent to the seller when he is taken back the sold goods.

How do you record a returned transaction?

Record the Sales Return Transaction Debit sales returns and allowances by the selling price. Debit the appropriate tax liability account by the taxes collected on the original sale. Credit cash or accounts receivable by the full amount of the original sales transaction.