When a parent company uses the equity method?

Nathan Sanders

Nathan Sanders

When a parent company uses the equity method to account for investment in a subsidiary, the amortization expense entry recorded during the year is eliminated on a consolidation worksheet as a component of Entry I.

What method is used for investments in equity securities with 20% to 50% ownership?

Equity accounting is an accounting method for recording investments in associated companies or entities. The equity method is applied when a company’s ownership interest in another company is valued at 20–50% of the stock in the investee.

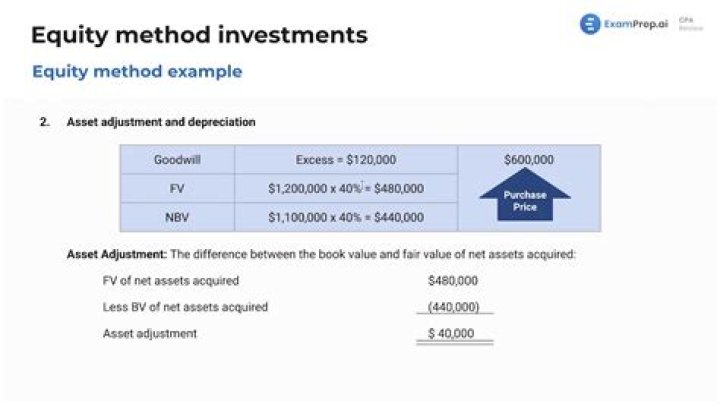

When an investor using the equity method pays more than its share of the investee’s book value the difference is?

These gains and expenses are expressed in the investee’s financial statements. The income statement represents any benefit or loss that the investing company makes. 34. When an investor, using the equity method, pays more than its share of the investee’s book value, the difference isa) ignored.

When an investor uses the equity method?

1. When an investor uses the equity method to account for investments in common stock, cash dividends received by the investor from the investee should be recorded asA deduction from the investor’s share of the investee’s profits.

What’s the difference between equity method and consolidation?

Consolidating the financial statements involves combining the firms’ income statements and balance sheets together to form one statement. The equity method does not combine the accounts in the statement, but it accounts for the investment as an asset and accounts for income received from the subsidiary.

Where does equity investment go on the balance sheet?

Equity method investments are recorded as assets on the balance sheet at their initial cost and adjusted each reporting period by the investor through the income statement and/or other comprehensive income ( OCI ) in the equity section of the balance sheet.

How do you calculate equity income?

Equity Income is calculated by adding up a shareholder’s dividend payouts for a year, along with the capital gains made from stock sales….Equity Income Calculation

- Review Your Investment Statements.

- Add up Income from Dividends.

- Add in Capital Gains.

- Equity = Dividends + Capital Gains.

When the investor properly discontinue the use of equity method?

The investor ordinarily should discontinue applying the equity method when the investment (and net advances) is reduced to zero and should not provide for additional losses unless the investor has guaranteed obligations of the investee or is otherwise committed to provide further financial support for the investee.

What are some general criticisms of the equity method for investments?

What are some general criticisms of the equity method for investments in the ownership shares of another firm? – significant influence and control may not be properly defined by existing quantitative guidelines.

What is the cost method of consolidation?

The consolidation method is a type of investment accounting. Under the consolidation method, a parent company combines its own revenue with 100% of the revenue of the subsidiary. Learn more about the various types of mergers and amalgamations. In accounting, it refers to the combination of financial statements..

Which investments are recorded using equity method?

Typically, equity accounting–also called the equity method–is applied when an investor or holding entity owns 20–50% of the voting stock of the associate company. The equity method of accounting is used only when an investor or investing company can exert a significant influence over the investee or owned company.

Why would a company use the equity method?

One of the most notable advantages of the Equity Method is its ability to enable the investor to record, show and prove a more truthful and realistic balance of income. The income on the sheet shows all earnings from all investments, not solely from the main company.

When an equity method investment account is reduced to zero balance?

Question: When an equity method investment account is reduced to a zero balance Multiple Choice The investor should establish a negative investment account balance for any future losses reported by the investee. The investor should discontinue using the equity method until the investee begins paying dividends.