When a perfectly competitive firm is in short run equilibrium?

Isabella Wilson

Isabella Wilson

Equilibrium in perfect competition is the point where market demands will be equal to market supply. A firm’s price will be determined at this point. In the short run, equilibrium will be affected by demand. In the long run, both demand and supply of a product will affect the equilibrium in perfect competition.

When a perfectly competitive industry is in long run equilibrium?

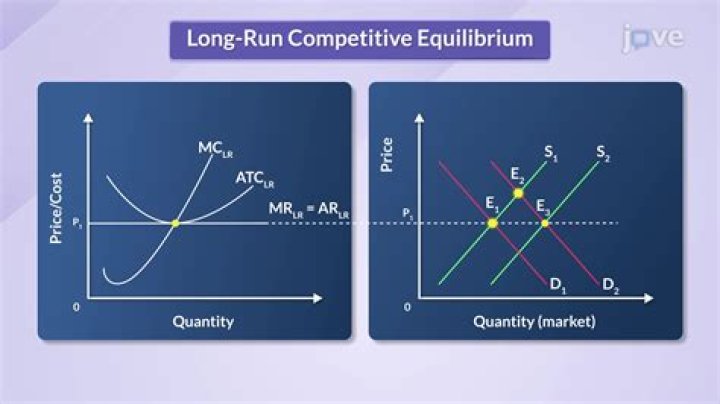

In a perfectly competitive market, long-run equilibrium will occur when the marginal costs of production equal the average costs of production which also equals marginal revenue from selling the goods.

How can we find the short run equilibrium for a firm under perfect competition?

For example, as we have seen in Fig. 10.5, the equilibrium (p = SMC) quantity of output produced and supplied by the firm at p = p1 is q = q1. Therefore, the short-run supply (SRS) of the firm at p = p1 is q = q1, and the point E1 (p1, q1) on the SMC curve is also a point on the firm’s SRS curve.

How is the short run price determined in a perfectly competitive market?

Short-run price is determined by short-run equilibrium between demand and supply. Supply curve in the short run under perfect competition is a lateral summation of the short-run marginal cost curves of the firm.

When there is short period equilibrium in perfect competition the following situations are possible?

Three Possibilities in Short-run In a perfectly competitive market, a firm can earn a normal profit, super-normal profit, or it can bear a loss. At the equilibrium quantity, if the average cost is equal to the average revenue, then the firm is earning a normal profit.

What is the difference between long-run and short run equilibrium?

We can compare that national income to the full employment national income to determine the current phase of the business cycle. An economy is said to be in long-run equilibrium if the short-run equilibrium output is equal to the full employment output.

What is short-run equilibrium?

Definition. A short run competitive equilibrium is a situation in which, given the firms in the market, the price is such that that total amount the firms wish to supply is equal to the total amount the consumers wish to demand.

How do you determine long-run and short-run equilibrium?

(1) In equilibrium, its short-run marginal cost (SMC) must equal to its long-run marginal cost (LMC) as well as its short-run average cost (SAC) and its long-run average cost (LAC) and both should be equal to MR=AR-P.

What is short run equilibrium output?

An economy is said to be in short run equilibrium when the level of aggregate output demanded is equal to the level of aggregate output supplied. …

How do you find the short run equilibrium quantity?

Example

- The short run supply function for each firm is. if p < 20.

- Thus the aggregate supply (given that there are 50 firms) is.

- The aggregate demand is Qd(p) = 280 p.

- The equilibrium price satisfies the equation 25p 500 = 280 p if the solution of this equation is at least 20.

- The output of each firm is (1/2)(30) 10 = 5.

Who determines price in a perfectly competitive market?

Price is determined by the intersection of market demand and market supply; individual firms do not have any influence on the market price in perfect competition. Once the market price has been determined by market supply and demand forces, individual firms become price takers.

How do you find the short-run equilibrium quantity?

How do you solve competitive equilibrium?

For every price, find the number of sellers whose costs (“reservation values”) are less than the price (so that they are willing to sell). Find the price at which the number of buyers willing to buy is equal to the number of sellers willing to sell. This price is a competitive equilibrium price.

What is the long-run equilibrium real GDP?

If an economy is said to be in long-run equilibrium, then Real GDP is at its potential output, the actual unemployment rate will equal the natural rate of unemployment (about 6%), and the actual price level will equal the anticipated price level.

How do you find short-run equilibrium?

An economy is in short-run equilibrium when the aggregate amount of output demanded is equal to the aggregate amount of output supplied. In the AD-AS model, you can find the short-run equilibrium by finding the point where AD intersects SRAS.

Is equilibrium always at an optimal level of output?

Yes, the equilibrium is always at an optimal level of output since at this point the demand is always equal to the supply in the market. Explanation: The optimum level of output is when the aggregate supply of output is equal to the aggregate demand of the output.

How do you know if its short-run or long-run?

“The short run is a period of time in which the quantity of at least one input is fixed and the quantities of the other inputs can be varied. The long run is a period of time in which the quantities of all inputs can be varied.

How do you solve equilibrium output?

E=C+I+G+NX [Aggregate demand is the total of consumption, investment, government purchases, and net exports.] E=Y* [In equilibrium, total spending matches total income or total output.]