When does a C Corporation become a S corporation?

Joseph Russell

Joseph Russell

When a C corporation elects to become an S corporation, S status begins on the day following the last day of the electing C corporation’s tax year. For an existing C corporation that is converting to S status, the S election may be filed:

How are the shareholders of a S corporation taxed?

A variation on this approach would account for the fact that the shareholders of an S corporation are subject to income tax with respect to the corporation’s profits on a current basis, without regard to whether such profits have been distributed by the corporation.

How to determine the value of an S Corp?

The practice of “tax-affecting” may be applied under various hypotheses, transfer scenarios, and valuation methodologies. In brief, tax affecting seeks to account for the fact that the income and gain of an S corporation are generally not subject to Federal income tax at the level of the S corporation.

Are there any tax benefits to being a s-Corp?

As a business owner, there are some tax benefits to being structured as a S-Corp. The biggest one (that almost everyone knows) is the potential to reduce/minimize their employment taxes. But did you know that through some deliberate and diligent tax planning, you could be able to legally reduce your tax burden further?

How is the financial year of a newly incorporated company defined?

Financial Year in case of newly incorporated company under New Act. The financial year of any company or body corporate has been defined under Section 2 (41) of the New Act, as under-

When do you need to file an initial return for an S corporation?

For example, if you formed your corporation and immediately elected S Corporation status in July 2011 but the company sat idle until April of the following year, you could file an initial tax return that includes the first 18 months. Your fiscal year would run from April 1 through March 31.

When was the first AGM of a newly incorporated company?

Financial year and First Annual General Meeting (AGM) of newly incorporated Company. Under the Companies Act, 1956 (‘Old Act’), it was open to the Companies to determine any period as their financial year (for example- 1st April to 31st March or 01st January to 31st December).

When was the first year corporations were taxed?

Although the Act was ruled unconstitutional, it was replaced by a Tax Act in 1909. This was the first year that corporate taxes were levied. 14 The current system is more progressive, meaning high-earning corporations are taxed at higher rates.

When does the accounting reference date end for a limited company?

This is because they: end on the ‘accounting reference date’ that Companies House sets for the end of your company’s financial year – this is the last day of the month your company was set up If your company was set up on 11 May, its accounting reference date will be 31 May the following year.

When do the first accounts of a company end?

Your first accounts usually cover more than 12 months. This is because they: end on the ‘accounting reference date’ that Companies House sets for the end of your company’s financial year – this is the last day of the month your company was set up If your company was set up on 11 May, its accounting reference date will be 31 May the following year.

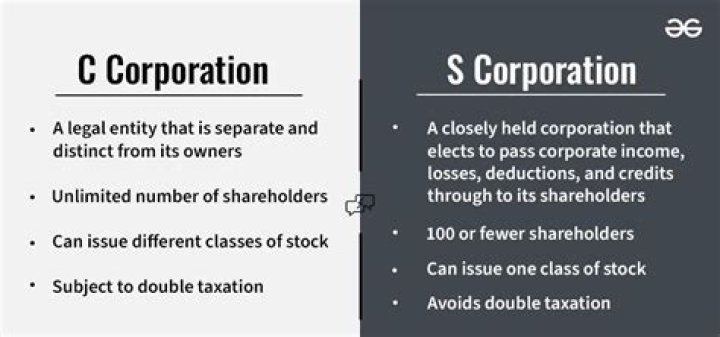

What makes a corporation file under the s Subchapter?

The key characteristic of a corporation filed under Subchapter S: It may pass business income, losses, deductions, and credits directly to shareholders, without paying any federal corporate tax—something known as a “pass-through” entity. It is liable on the corporate level for taxes on specific built-in gains and passive income, however.

What is a subchapter in the Internal Revenue Code?

A Subchapter S (S Corporation) is a form of corporation that meets specific Internal Revenue Code requirements. The requirements gives a corporation with 100 shareholders or fewer the benefit of incorporation while being taxed as a partnership.

What are the current developments in S corporations?

Other letter rulings excused terminations due to ineligible shareholders and allowed S corporations to reelect S status before five years had passed since a prior termination.