When should variance analysis be used?

Joseph Russell

Joseph Russell

This analysis is used to maintain control over a business through the investigation of areas in which performance was unexpectedly poor. For example, if you budget for sales to be $10,000 and actual sales are $8,000, variance analysis yields a difference of $2,000.

What is the objective of variance analysis cycle?

Variance Analysis deals with an analysis of deviations in the budgeted and actual financial performance of a company. The causes of the difference between the actual outcome and the budgeted numbers are analyzed to showcase the areas of improvement for the company.

What is variance analysis and its steps?

There are four steps involved in this process: Calculate the difference between what we spent and what we budgeted to spend. Investigate why there is a difference. Put the information together and talk to management. Put together a plan to get costs more in line with the budget.

How do you explain variance analysis?

Definition: Variance analysis is the study of deviations of actual behaviour versus forecasted or planned behaviour in budgeting or management accounting. This is essentially concerned with how the difference of actual and planned behaviours indicates how business performance is being impacted.

What is analysis variance explain with examples?

Analysis of variance, more commonly called ANOVA, is a statistical method that is designed to compare means of different samples. Essentially, it is a way to compare how different samples in an experiment differ from one another if they differ at all. This means that the error gets larger for every test you do.

What is variance in statistics with example?

We know that variance is a measure of how spread out a data set is. It is calculated as the average squared deviation of each number from the mean of a data set. For example, for the numbers 1, 2, and 3 the mean is 2 and the variance is 0.667. [(1 – 2)2 + (2 – 2)2 + (3 – 2)2] ÷ 3 = 0.667.

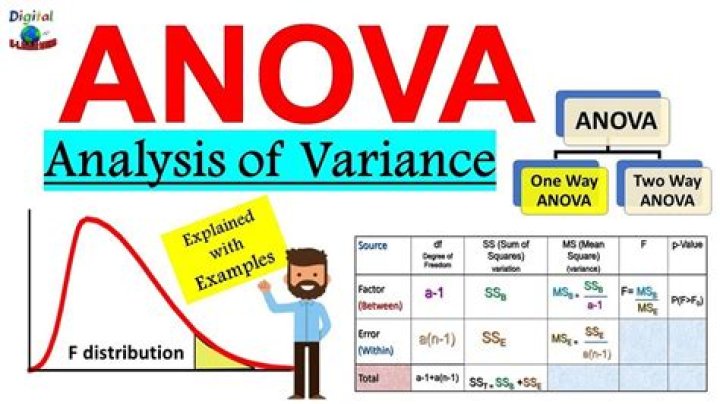

What are the three types of variance in an analysis of variance?

Analysis of variance/Types

| ANOVA models | Definitions |

|---|---|

| One-way ANOVA | Comparison of means of three or more independent groups. |

| One-way repeated measures ANOVA | Comparison of means of three or more within-subject variables. |

| Factorial ANOVA | Comparison of cell means for two or more between-subject IVs. |

What are different types of variance analysis?

Types of Variance (Cost, Material, Labour, Overhead,Fixed Overhead, Sales, Profit) If you haven’t been through Variance Analysis Introduction, please consider going through that before proceeding for better understanding.

How do we calculate variance?

How to Calculate Variance

- Find the mean of the data set. Add all data values and divide by the sample size n.

- Find the squared difference from the mean for each data value. Subtract the mean from each data value and square the result.

- Find the sum of all the squared differences.

- Calculate the variance.

Variance analysis is used to assess the price and quantity of materials, labour and overhead costs. These numbers are reported to management.

What is the purpose of a variance report?

A variance report is a document that compares planned financial outcomes with the actual financial outcome. In other words: a variance report compares what was supposed to happen with what happened. Usually, variance reports are used to analyze the difference between budgets and actual performance.

What are the types of Variance analysis?

Types of Variances which we are going to study in this chapter are:-

- Cost Variances.

- Material Variances.

- Labour Variances.

- Overhead Variance.

- Fixed Overhead Variance.

- Sales Variance.

- Profit Variance.

What does variance mean in a variance analysis?

Variance refers to the degree of fluctuation between the scheduled and actual performance. Therefore, Variance analysis refers to the detailed study of the difference between the planned or scheduled results with the actual results obtained. The variance analysis consists of two steps:

How are variances calculated in budgeting and forecasting?

Learn variance analysis step by step in CFI’s Budgeting and Forecasting course. When standards are compared to actual performance numbers, the difference is what we call a “variance.” Variances are computed for both the price and quantity of materials, labor, and variable overhead, and are reported to management.

Why is variance analysis important in cost accounting?

Some go to great lengths to improve direct labor price variance. One of the purposes of cost accounting is to hold people and things responsible for the costs they cause. Variance analysis plays a key role in this, but it goes deeper than I discussed in earlier chapters.

Why do you need subdividing in a variance analysis?

That involves subdividing variances based on their cause, and it’s a prerequisite for actionable information. A lot of the headache for students comes from having to subdivide variance into actionable chunks of information. But it’s also a critical component of variance analysis, without which the whole procedure would probably be worthless.