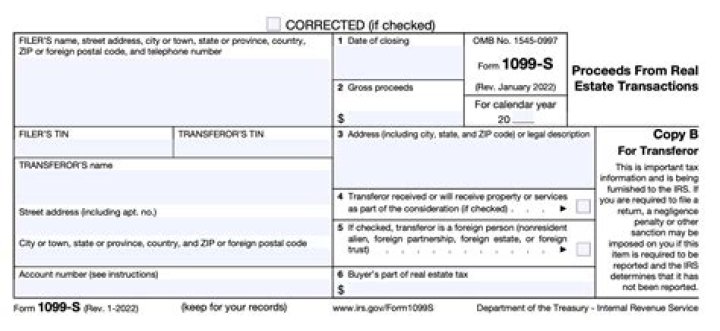

Where can I Find Form 1099 for sale of real estate?

Joseph Russell

Joseph Russell

On smaller devices, click in the upper left-hand corner, then click Federal. Click Investment Income to expand, click Gain or loss on the sale of investments to expand, then click Capital gain or loss (Form 1099-B). Click + Add Form 1099-B to create a new form or click Edit to review a form already created.

How to assist sellers in the completion of the 1099?

Each Seller must complete a 1099-S Certification form (Husband and Wife must each complete a separate form). Step 2 A) If all questions are answered “True or Yes” on the 1099-S Certification, return the completed and signed form to your Escrow officer.

What kind of transaction is required to be reported on Form 1099?

Generally, you are required to report a transaction that consists in whole or in part of the sale or exchange for money, indebtedness, property, or services of any present or future ownership interest in any of the following.

Can a joint seller file a Form 1099-S?

If there are joint sellers, you must obtain a certification from each seller (whether married or not) or file Form 1099-S for any seller who does not make the certification. The certification must be signed by each seller under penalties of perjury. A sample certification format can be found in Rev. Proc.

What do you need to know about Form 1099-S?

Sales or exchanges involving foreign transferors are reportable on Form 1099-S. For information on the transferee’s responsibility to withhold income tax when a U.S. real property interest is acquired from a foreign person, see Pub. 515, Withholding of Tax on Nonresident Aliens and Foreign Entities .

Can a substitute 1099-S form be used?

Do NOTsubmit the substitute 1099-S form that is generated in REsource (or any other substitute 1099-S form) to be delivered to the seller. Submitting a substitute 1099-S form to the IRS could result in severe penalties being imposed on the reporting person. For the requirements and formatting of the magnetic media, see IRS Publication 1220.