Which of the following underlies the application of generally accepted auditing standards?

Emily Baldwin

Emily Baldwin

Answer D is correct because generally accepted auditing standards (GAAS) deal with measures of the quality of the performance of audit procedures. Answer A is correct because the elements of materiality and audit risk underlie the application of all the standards, particularly the standards of fieldwork and reporting.

What is a good materiality threshold for an account?

Variable Size Rule Methods: 2% to 5% of gross profit (if less than $20,000) 1% to 2% of gross profit (if gross profit is more than $20,000 but less than $1,000,000) 0.5% to 1% of gross profit (if gross profit is more than $1,000,000 but less than $100,000,000.

Which sections requires a CPA to comply with generally accepted accounting principles and generally accepted auditing standards?

03 Rule 202, Compliance With Standards, of the AICPA Code of Profes- sional Conduct [ET section 202.01], requires an AICPA member who performs an audit (the auditor) to comply with standards promulgated by the ASB.

Which of the following best describes what is meant by generally accepted auditing standards 1 point?

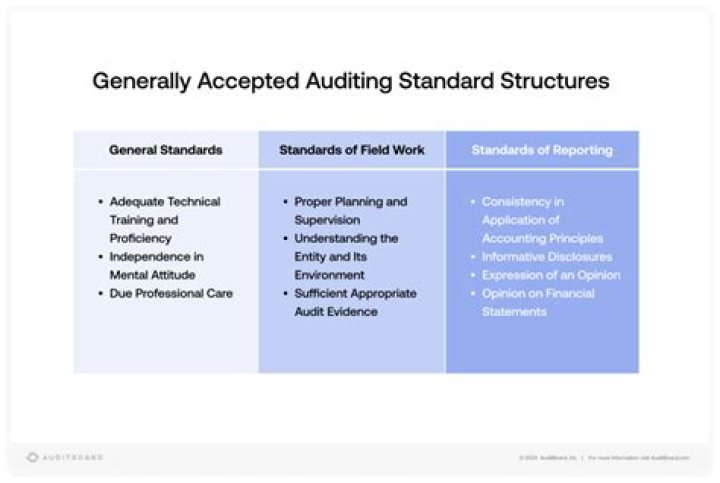

Which of the following best describes what is meant by the term generally accepted auditing standards? Measures of the quality of the auditor’s performance. Encompasses the conventions, rules, and procedures necessary to define U.S. accepted accounting practices at a particular time.

What is the risk of material misstatement?

The risk of material misstatement is the risk that the financial statements of an organization have been misstated to a material degree. Inherent risk is the susceptibility of an assertion to misstatement because of error or fraud, before considering controls.

What does GAAS stand for?

Generally accepted auditing standards

Generally accepted auditing standards (GAAS) are a set of systematic guidelines used by auditors when conducting audits on companies’ financial records. GAAS helps to ensure the accuracy, consistency, and verifiability of auditors’ actions and reports.

Can auditors reduce inherent risk?

Inherent and control risk combine to form the risk of material misstatement, or RMM. These risks exist independent of the auditor and cannot be reduced through substantive procedures.

How do you calculate materiality?

The research study also cites KPMG’s formula-based method: Materiality = 1.84 times (the greater of assets or revenues)2/3….Single rule methods:

- 5% of pre-tax income;

- 0.5% of total assets;

- 1% of equity;

- 1% of total revenue.

How do you explain materiality?

In accounting, materiality refers to the relative size of an amount. Relatively large amounts are material, while relatively small amounts are not material (or immaterial). Another view of materiality is whether sophisticated investors would be misled if the amount was omitted or misclassified.

How is materiality percentage calculated?

The materiality threshold is defined as a percentage of that base. The most commonly used base in auditing is net income (earnings / profits). Most commonly percentages are in the range of 5 – 10 percent (for example an amount <5% = immaterial, > 10% material and 5-10% requires judgment).

What is the standard for materiality?

The standard for materiality articulated by the Supreme Court — “an omitted fact is material if there is a substantial likelihood that a reasonable shareholder would consider it important in deciding how to vote” — benefits investors in at least three ways.

What is a good materiality threshold?

Most commonly percentages are in the range of 5 – 10 percent (for example an amount <5% = immaterial, > 10% material and 5-10% requires judgment).

What percentage should performance materiality be?

Usually performance materiality is calculated at 50% to 75% of materiality. Why the range? Different risk levels for different clients. If you believe the risk of undetected misstatements is high, then use a lower percent (e.g., 55% of materiality).

What is the overall review stage of an audit?

The overall review would generally include reading the financial statements and notes and considering (a) the adequacy of evidence gathered in response to unusual or unexpected balances identified in planning the audit or in the course of the audit and (b) unusual or unexpected balances or relationships that were not …

How is materiality calculated?

To establish a level of materiality, auditors rely on rules of thumb and professional judgment. They also consider the amount and type of misstatement. The materiality threshold is typically stated as a general percentage of a specific financial statement line item.

How is materiality determined?

Auditors usually determine the performance materiality based on the level of risks that are involved in the audit. While overall materiality is for financial statements as a whole, performance materiality is the materiality for particular classes of transactions, account balances, or disclosures.

Is performance materiality based on risk?

First of all, materiality refers to the idea that a single misstatement in the financial statements of a business can affect the ability of users to make economic decisions based on those financial statements. In contrast, auditors set performance materiality based on the assessment of audit risk.