Who is considered the account owner of an Education IRA?

Emily Baldwin

Emily Baldwin

While your child is the beneficiary of the Coverdell ESA, you are the owner of the account. Although you must use the funds to cover your child’s educational expenses, your kiddo does not get control of the fund at any point.

How are educational IRAS taxed?

The funds in an education IRA can be withdrawn tax-free when they are needed for educational purposes. That investment grows free of federal taxes, and withdrawals are tax-free as well, as long as certain requirements are met related to the year’s contributions are made and the year’s withdrawals are made.

Can I use my IRA for tuition?

Money in an IRA can be withdrawn early to pay for tuition and other qualified higher education expenses for you, your spouse, children, or grandchildren—without penalty. To avoid paying a 10% early withdrawal penalty, the IRS requires proof that the student is attending an eligible institution.

Can you tap an IRA to pay for Education?

If you decide to tap your IRA early in order to pay for education costs, you will want to avoid these four mistakes that others have made. Wrong Tuition Bill. A father took a distribution from his IRA to pay his son’s tuition at a private high school. He argued that this qualified for the exception to the penalty.

What is the definition of an education IRA?

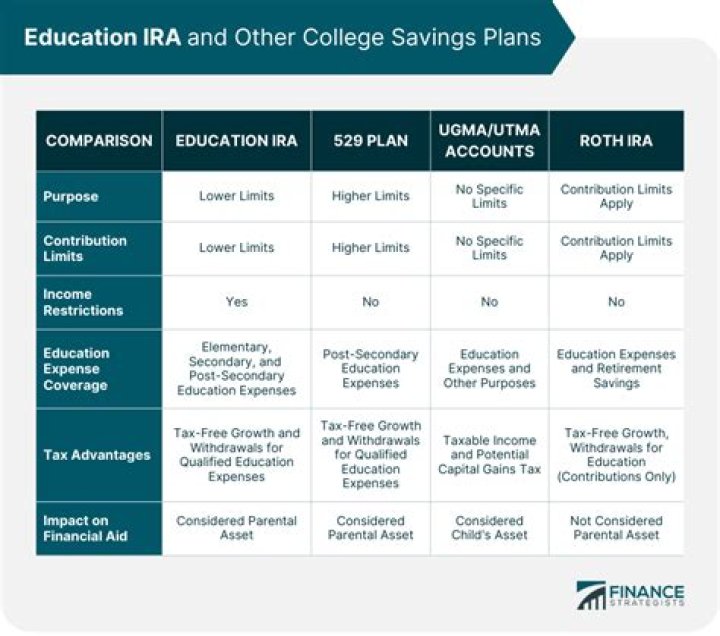

DEFINITION of ‘Education IRA’. An education IRA is a tax-advantaged investment account for higher education now more formally known as a Coverdell Education Savings Account (ESA).

When did Coverdell change the name to an education IRA?

Education IRAs existed before they were renamed Coverdell ESAs in 2002 and were made even more attractive as an educational savings vehicle when the list of qualified expenses was extended to certain K-12 expenses.

How old do you have to be to open an education IRA?

An education IRA is a tax-advantaged investment account for higher education, now more formally known as a Coverdell Education Savings Account (ESA). Under this educational savings vehicle, parents and guardians are allowed to make non-deductible contributions to an education individual retirement account (IRA) for a child under the age of 18.