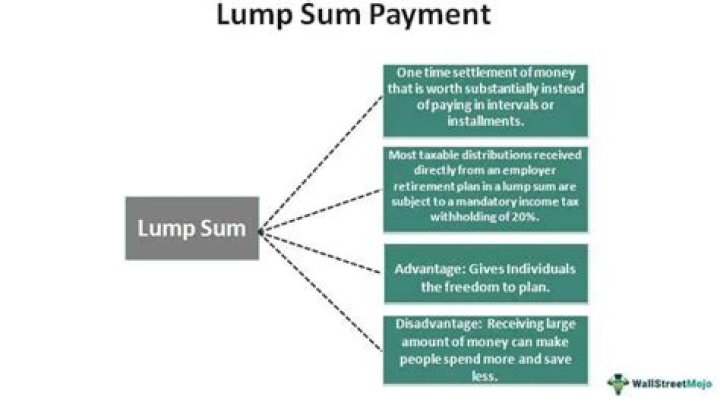

Why would a retiring employee accept a lump sum payment from the employer instead of ongoing pension payments?

Sophia Bowman

Sophia Bowman

Employers have various reasons. They may use it as an incentive for older, higher-cost workers to retire early. Or they may make the offer because eliminating pension payments generates accounting gains that boost corporate income.

Can pensioners take lump sum from work?

In most schemes you can take 25 per cent of your pension pot as a tax-free lump sum. You’ll then have 6 months to start taking the remaining 75 per cent – you can usually: get regular payments (an ‘annuity’) invest the money in a fund that lets you make withdrawals (‘drawdown’)

Do you get a lump sum pension when you retire?

You may have a vested benefit from a former employer, or your current company may be offering you a pension lump-sum buyout long before you retire.

Do you need advice on roll over for this lump sum payment?

I need advice on roll over for this lump sum payment.” I’m assuming that the writer is over age 59 1/2, but the information provided will also apply if you’re younger. Typically, when you leave an employer that offers a traditional pension plan, you’re given several options as to how to handle the proceeds:

What happens to my taxes when I take a lump sum?

If you take monthly income, your payments are subject to ordinary income tax. If you take a lump sum in cash, it’s immediately taxable, and you’ll be subject to 20 percent federal (and potentially state) mandatory tax withholding. With a few exceptions, distributions taken prior to age 59½ are subject to a 10 percent IRS early withdrawal penalty.

Is it better to take a lump sum or a cash out?

A lump-sum payment may seem attractive. You give up the right to receive future monthly benefit payments in exchange for a cash-out payment now—typically, the actuarial net present value of your age-65 benefit, discounted to today. Taking the money up front gives you flexibility.