Can a co borrower repossess a car?

Emily Baldwin

Emily Baldwin

Usually, when you cosign a car loan, you agree to be responsible for the debt if the primary debtor does not make payments or otherwise defaults on the loan. If the primary debtor defaults on the loan, then the creditor has the right to repossess the car, sell it and pursue you for the deficiency.

How long does a finance company have to repossess a car?

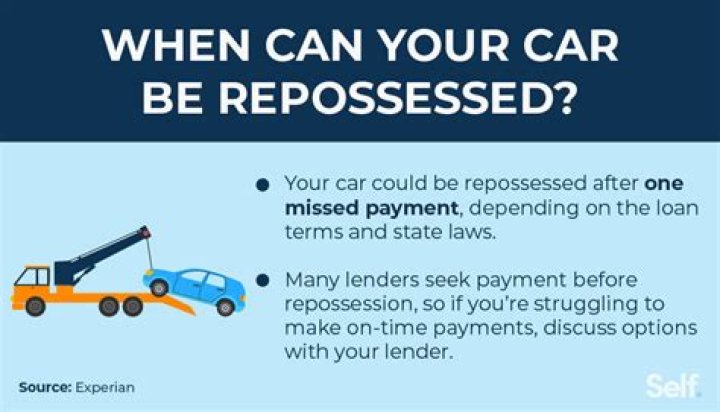

Common Myths About Car Repossession Myth #1 – Car finance companies have to wait until you are at least 3 months behind on your payments before they can repossess your car. Truth – Car finance companies have the legal right to repossess your vehicle even if you are just one day late paying your bill.

Does a cosigner have rights to the car?

Cosigners don’t have any rights to your vehicle, so they can’t take possession of your car – even if they’re making the payments. What a cosigner does is “lend” you their credit in order to help you get approved for an auto loan. A cosigner must have good credit and agree to make any payments in case you’re unable to.

Can the co buyer take the car?

The co-buyer’s rights to the vehicle allow the co-buyer to take possession of the car if you fail to pay — and even if you don’t, because you’re equal owners — and you’ll need the co-buyer’s permission to sell the car later. A cosigner has no ownership rights but might be harder to find.

What rights does a co borrower have?

Co-borrowers share responsibility for repayment in the eyes of the lender, just as cosigners do. If co-borrowers take out a joint loan to buy an asset, they also usually both have a legal right to the asset, in addition to a legal responsibility for paying for it.

How do I get a co borrower off my car?

Fear not, as there are two main ways to remove your name from a joint auto loan: refinancing or selling the vehicle.

- Refinancing. If the other co-borrower wants to keep the car and you want your name removed from the loan, they can try to qualify for refinancing.

- Sell the car.

Can a bank revoke a loan on a car after I signed the contract?

Depending on your contract, a bank or dealership could revoke your loan even after you’ve signed a contract. If you’ve financed your new car at the dealership, they could also deny your financing after you’ve driven the car off the lot.

Can you sue for car payment?

If you are sued, don’t ignore it. A default judgment could be entered against you for the balance of your car loan, which in turn could lead actions such as bank account garnishment, property liens, or in some states, wage garnishment.

How do I get a co-borrower off my car?

Can a buyer remove a co-buyer?

If the lender is to remove the co-buyer, you will need to refinance the loan on your own. If the lender doesn’t permit any modification then you have the option of taking out another loan to pay off the car loan in full. Once the car loan is repaid in full then both parties are relieved of their obligation.

Does it matter who is borrower and co-borrower?

Cosigners are people who guarantee debt for someone who cannot qualify on their own. The understanding is that the primary borrower is the person legally responsible for repaying what is owed….Cosigner vs. co-borrower: Summary.

| Co-borrower | Cosigner |

|---|---|

| Takes on shared debt with someone else | Guarantees debt for someone else |

What rights does a co-borrower have?

Can you cancel a car deal after signing?

Canceling a deal after you have signed the papers is not easy. Though some transactions include a three-day right to cancel or a right to rescind, this not a legal requirement for vehicle transactions, and is usually at the discretion of the seller.

Can you be a month behind on your car payment?

Typically, most lenders wait until you are about 3 months behind on car payments. Although you can be considered in default after 30 days, lenders may wait 90-120 days before taking action. In addition to an added sense of uncertainty, repossessions also leave a negative mark on your credit history.

When you default on a vehicle loan, the lender may repossess the vehicle by force to recover the debt. In most cases, either the primary borrower or the co-borrower can authorize a lender to repossess a vehicle if the loan is in default.

What are the repossession laws in Colorado?

In Colorado, the lender must wait until the debtor is in default for at least 10 days before the lender can send a “right to cure” the default. A “right to cure” simply informs you of your opportunity to make up the missed payments and stop the repossession process in its tracks.

Can the primary borrower take the car from the co-borrower?

Cosigners can’t take possession of the vehicle they cosign for, or remove the primary borrower from the loan, since their name isn’t on the vehicle’s title. Getting out of an auto loan as a cosigner isn’t always easy. However, knowing what you signed on for as a cosigner is key and you’re not out of options.

Can a co-borrower request my car be repossessed?

If you are behind in the payments, either one of you can surrender the vehicle to the lender or authorize a repossession. If the lender makes the decision to repossess on his own, neither one of you can prevent him from doing so.

Who is responsible for the repossession of a car?

In the event the primary borrower cannot pay, the cosigner is legally responsible for paying off the debt. Should the bank repossess the car as a result of missed payments, the cosigner’s credit report will reflect the missed payments and, ultimately, the repossession.

What happens to a cosigner when a car is repossessed?

When someone becomes a cosigner, they sign the loan contract and share responsibility. If the primary borrowers fails to make payments, the lender can demand that the cosigner make them. If the primary borrower defaults on the loan, the repossession is also going to affect the cosigner’s credit score, because you share responsibility as a cosigner.

Can a creditor use physical force to repossess a car?

That is, the creditor can’t use or threaten to use physical force against you to repossess the property. If the creditor or its agent breaches the peace during a repossession, like by pushing you aside and breaking into your locked garage to repossess your vehicle, you can file a lawsuit against that creditor.