Can personal loan interest be claimed on taxes?

David Craig

David Craig

Section 24(b) of the Income Tax Act, 1961, allows for a tax rebate on personal loan if the amount is used for home renovation or improvement. In this case, interest paid on personal loan repayment up to Rs. 30,000 can be claimed as deduction from the total taxable income. 2 lakh is allowed for the interest paid.

Can you claim tax back on car finance?

Regardless of the method used to purchase the vehicle, the initial cost or finance costs are not tax deductible when you acquire a vehicle personally. Additionally you will not be able to claim tax relief on running costs such as road tax, insurance, fuel and servicing.

What kind of loans are tax deductible?

Types of interest that are tax deductible include mortgage interest for both first and second (home equity) mortgages, mortgage interest for investment properties, student loan interest, and the interest on some business loans, including business credit cards.

What kind of interest is tax deductible?

According to the IRS, only a few categories of interest payments are tax-deductible: Interest on home loans (including mortgages and home equity loans) Interest on outstanding student loans. Interest on money borrowed to purchase investment property.

Does buying a car affect your taxes?

If you buy a vehicle in California, you pay a 7.5 percent state sales tax rate regardless of the vehicle you buy. The collection of sales tax from vehicles is $3 billion more than state income taxes and $2 billion more than sales tax from used car purchases.

Do you get tax break for buying a car?

There is a general sales tax deduction available if you itemize your deductions. You can deduct sales tax on a vehicle purchase, but only the state and local sales tax. You’ll only want to deduct sales tax if you paid more in state and local sales tax than you paid in state and local income tax.

Is giving a loan tax deductible?

Though personal loans are not tax deductible, other types of loans are. Interest paid on mortgages, student loans, and business loans often can be deducted on your annual taxes, effectively reducing your taxable income for the year.

What qualifies as a tax deduction?

You subtract deductions from your gross income and sometimes, you’ll end up in a lower tax bracket as a result. Popular tax deductions include the student loan interest deduction, the medical expenses deduction, the IRA contributions deduction and the self-employment expenses deduction.

What interest is tax deductible in 2020?

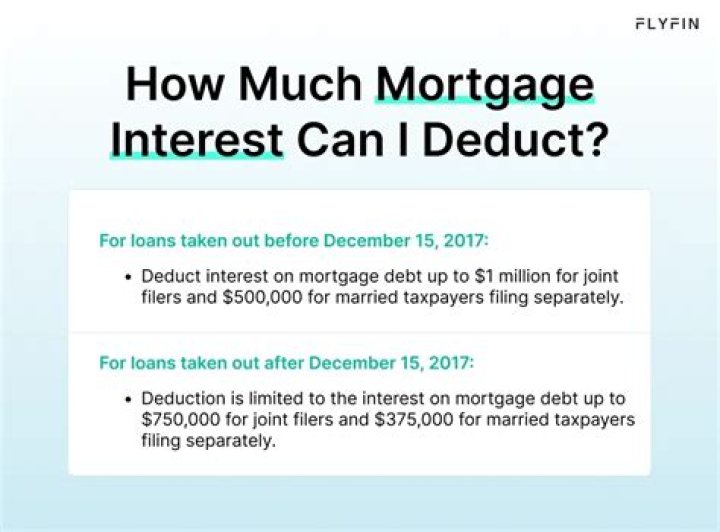

The 2020 mortgage interest deduction Mortgage interest is still deductible, but with a few caveats: Taxpayers can deduct mortgage interest on up to $750,000 in principal.

How do you write off a car purchase on your taxes?

Tax Write-Off of Car Purchase If you buy a car that you intend to use for business, you can write off some of the purchase price with the federal Section 179 deduction. You usually write off business purchases through depreciation, but Section 179 allows you to deduct the entire amount upfront.

Can you give a family member an interest-free loan?

The IRS will deem any forgone interest on an interest-free loan between family members as a gift for federal tax purposes, regardless of how the loans are structured or documented. There are some exceptions when the AFR is not required to be charged on a loan.

What can you deduct if you take standard deduction?

If you take the standard deduction on your 2020 tax return, you can deduct up to $300 for cash donations to charity you made during the year. (For 2020 joint returns, the amount allowed is still only $300.) Donations to donor advised funds and certain organizations that support charities are not deductible.

Can I deduct property taxes if I take the standard deduction?

The standard deduction is a specified dollar amount you are allowed to deduct each year to account for otherwise deductible personal expenses such as medical expenses, home mortgage interest and property taxes, and charitable contributions.

What is the new refundable tax credit for 2020?

Refundable tax credits For example, if a taxpayer owes $1,000 in federal income tax in 2020 and has a $3,000 refundable tax credit, that additional $2,000 can be paid to them in the form of a tax refund. On the other hand, a non-refundable credit can be used to reduce tax liability to zero, but not beyond that point.

How much can you write off for vehicle purchase?

How much can you write off for a vehicle purchase? If the vehicle is for personal use, you could write off car sales and property tax up to the federal or state maximum. The federal maximum allows you to deduct up to $10,000 total in sales, income and property tax deductions ($5,000 total if married filing separately).

How do I report interest on family loan?

The federal income tax results are straightforward if your loan charges an interest rate that equals or exceeds the AFR. You must report the interest income on your Form 1040. The borrower (your relative) may or may not be able to deduct the interest, depending on how the loan proceeds are used.

Can I lend money without interest?

A no-interest loan means you are only paying back the principal — or the money you borrowed from the lender — without interest. But you’ll still want to be mindful if your loan includes any additional costs, like an origination fee.

What personal expenses are tax deductible?

Mortgage Interest.