How do you prepare a profit and loss?

Isabella Wilson

Isabella Wilson

How to write a profit and loss statement

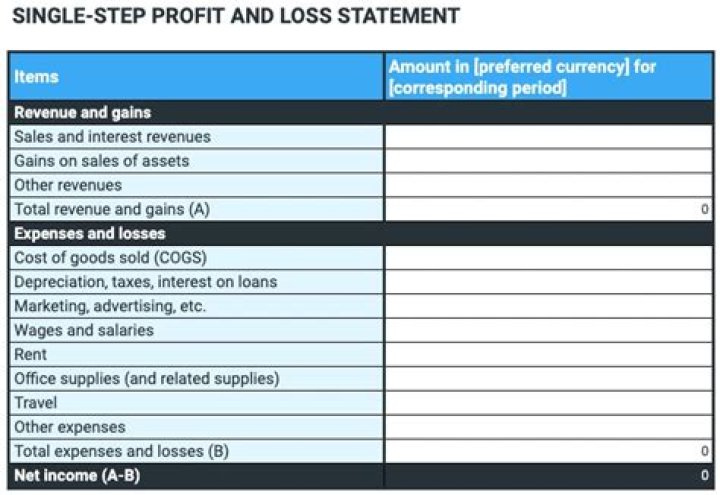

- Step 1: Calculate revenue.

- Step 2: Calculate cost of goods sold.

- Step 3: Subtract cost of goods sold from revenue to determine gross profit.

- Step 4: Calculate operating expenses.

- Step 5: Subtract operating expenses from gross profit to obtain operating profit.

How would you explain a profit loss?

A profit and loss statement is calculated by taking a company’s total revenue and subtracting the total expenses, including tax. If the resulting figure – known as net income – is negative, the company has made a loss, and if it is positive, the company has made a profit.

What should one look for in a profit and loss account?

Below are a list of some of the easiest yet effective things to analyze in your profit and loss statement:

- Sales.

- Sources of Income or Sales.

- Seasonality.

- Cost of Goods Sold.

- Net Income.

- Net Income as a Percentage of Sales (also known a profit margin)

How do you talk about P&L?

- Define the period for your profit and loss statement.

- Discuss your net sales figure.

- Provide a breakdown of your costs of goods sold applicable to businesses that sell products.

- Explain your expenses section, which may make up the majority of your profit and loss statement.

How do you manage P&L?

What is P&L management?

- Create P&L statements. First, create profit and loss statements.

- Compare P&L statements. Once you have your profit and loss statement for each accounting period, you can make comparisons.

- Make changes to business finances.

- Meet with an accountant.

When do I need to prepare a profit and loss statement?

This statement shows the revenues and expenses of the business, and resulting profit or loss, over a specific time period (a month, a quarter, or a year). When Do I Need to Prepare a Profit and Loss Statement? Periodic P&L. Every business needs to prepare and review its profit and loss statement periodically – at least every quarter.

What is the formula for a profit and loss report?

The basic formula of a P&L report is: Revenue – Expenses = Profits What Does the Profit and Loss Statement Show? The profit and loss report is an important financial statement used by business owners and accountants.

How to answer a profit and loss question?

Here is a question I recently received from one of my customers about how to answer a financial question: If playback doesn’t begin shortly, try restarting your device. Videos you watch may be added to the TV’s watch history and influence TV recommendations. To avoid this, cancel and sign in to YouTube on your computer.

How many quarters should a profit and loss statement cover?

If you’re preparing the statement for a third party, they may dictate the period of time the statement should cover. A profit and loss statement typically should cover at least one quarter to convey any significant degree of helpful information.