Is theft an itemized deduction?

Nathan Sanders

Nathan Sanders

Individuals may claim their casualty and theft losses as an itemized deduction on Schedule A (Form 1040), Itemized Deductions (or Schedule A (Form 1040NR) PDF, if you’re a nonresident alien). Report casualty and theft losses on Form 4684, Casualties and Thefts PDF.

Is a theft loss tax deductible?

Casualty and theft losses are deductible losses that arise from the destruction or loss of a taxpayer’s personal property. To be deductible, casualty losses must result from a sudden and unforeseen event. Theft losses generally require proof that the property was actually stolen and not just lost or missing.

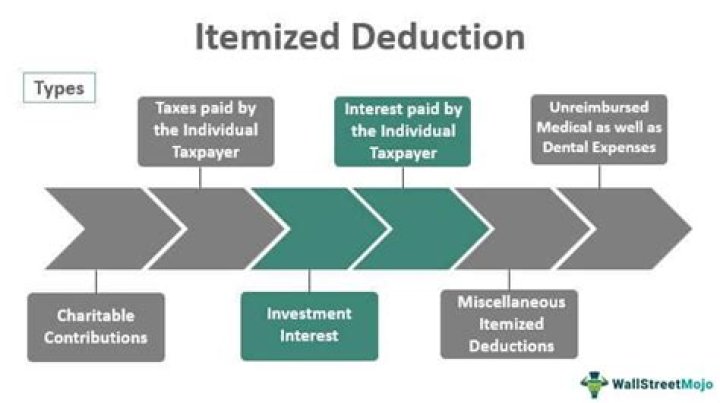

What are the rules for itemized deductions on taxes?

Many rules concerning itemized deductions are beyond the scope of this article. Working with an experienced and competent tax preparer can help to ensure those rules are applied to your tax return. Your tax preparer should also be able to allow you to determine whether you should itemize or take the standard deduction.

Where do theft losses go on a federal tax return?

The line on Form 1040 is different, however, beginning with the 2018 tax year. The IRS has revised Form 1040, effective as of the 2019 filing season, and for tax year 2018, itemized deductions or the standard deduction are entered on line 8 of the 1040. Do Theft Losses Qualify?

Do you have to itemize to claim loss on taxes?

First, you must itemize to claim this deduction. You can’t claim the standard deduction for your filing status and still claim the losses. There are a few other requirements as well. This deduction used to cover a pretty wide-ranging set of circumstances, but that changed with the passage of the Tax Cuts and Jobs Act (TCJA) in December 2017.

How is the casualty and theft loss deduction calculated?

Calculating the Casualty Loss Deduction. Casualty and theft losses are limited to a $100 threshold per loss event and an overall threshold of 10 percent of your adjusted gross income. They do not include any property that is covered by insurance if the insurance company reimburses you for the loss.