Is weighted average inventory GAAP?

David Craig

David Craig

One of the most basic differences is that GAAP permits the use of all three of the most common methods for inventory accountability—weighted-average cost method; first in, first out (FIFO); and last in, first out (LIFO)—while the IFRS forbids the use of the LIFO method.

Is FIFO a GAAP?

There are no GAAP or IFRS restrictions on the use of FIFO in reporting financial results. IFRS does not all the use of the LIFO method at all.

Is weighted average a stock valuation method?

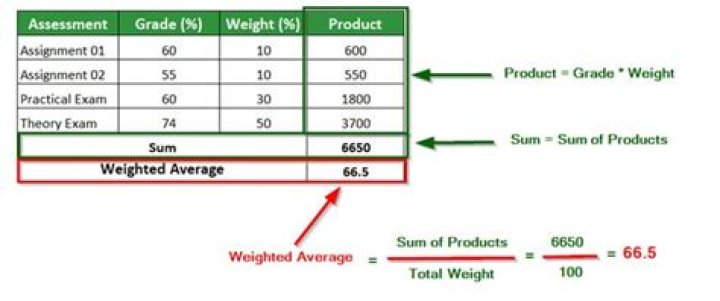

Inventory weighted average (also known as ‘weighted average cost’) is one of the four most common inventory valuation methods used in ecommerce accounting. This method uses a weighted average to determine the amount of money that goes into COGS and inventory.

Why does US GAAP allow LIFO?

LIFO is allowed in the US because it is a quick and dirty approximation to inflation accounting for the income statement. However, its use messes up the balance sheet and allows LIFO dipping to occur – which completely messes up the income statement for the period in which it occurs.

Does US GAAP allow LIFO?

LIFO is prohibited under IFRS and ASPE. However, under the US Generally Accepted Accounting Principles (GAAP), it is permitted.

How is weighted average cost used in inventory valuation?

The weighted average cost (WAC) method of inventory valuation uses a weighted average to determine the amount that goes into COGS and inventory. The weighted average cost method divides the cost of goods available for sale by the number of units available for sale. The WAC method is permitted under both GAAP and IFRS.

How does the WAC method of inventory valuation work?

In accounting, the Weighted Average Cost (WAC) method of inventory valuation uses a weighted average to determine the amount that goes into COGS

What is weighted average cost ( WAC ) in accounting?

What is Weighted Average Cost (WAC)? In accounting, the Weighted Average Cost (WAC) method of inventory valuation uses a weighted average to determine the amount that goes into COGS

How are inventories measured on a GAAP basis?

Under US GAAP, inventories are measured at the lower of cost, market value, or net realisable value depending upon the inventory method used. Market value is defined as current replacement cost subject to an upper limit of net realizable value and a lower limit of net realizable value less a normal profit margin.