What do write offs mean?

Robert Harper

Robert Harper

A write-off is an accounting action that reduces the value of an asset while simultaneously debiting a liabilities account. It is primarily used in its most literal sense by businesses seeking to account for unpaid loan obligations, unpaid receivables, or losses on stored inventory.

What write offs can I use 2020?

These are common above-the-line deductions to know for 2020:

- Alimony.

- Educator expenses.

- Health savings account contributions.

- IRA contributions.

- Self-employment deductions.

- Student loan interest.

- Charitable contributions.

Can I write-off Internet if I work from home?

Since an Internet connection is technically a necessity if you work at home, you can deduct some or even all of the expense when it comes time for taxes. You’ll enter the deductible expense as part of your home office expenses. Your Internet expenses are only deductible if you use them specifically for work purposes.

What can I write-off on my taxes if I work from home?

For example, if your home office is one-tenth of the square footage of your house, you can deduct 10% of the cost of your mortgage interest or rent, utilities (such as electric, water and gas bills) and homeowners insurance. You can also deduct 10% of other whole-house expenses, such as cleaning and exterminator fees.

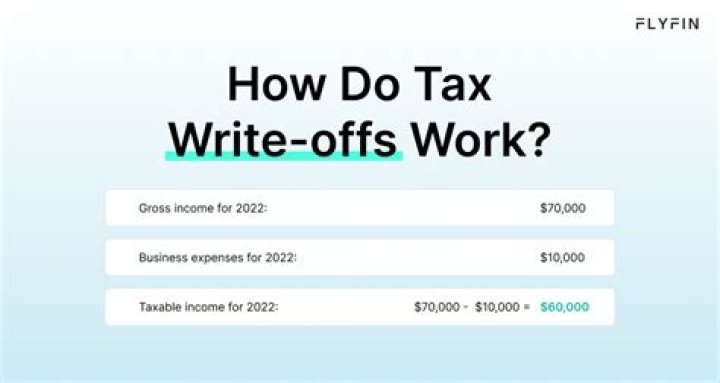

Which is an example of a business write off?

For income tax purposes, write offs are business expenses that are subtracted from revenue to find total taxable revenue. For example, a freelance interior designer can claim car mileage as a tax deduction since she needs to travel to meet clients. What Are Business Write Offs?

What are the three most common write off scenarios?

Three of the most common scenarios for business write-offs include unpaid bank loans, unpaid receivables, and losses on stored inventory. Financial institutions use write-off accounts when they have exhausted all methods of collection action.

What’s the difference between a write-off and a loss?

Write-offs may be tracked closely with an institution’s loan loss reserves, which is another type of non-cash account that manages expectations for losses on unpaid debts. Loan loss reserves work as a projection for unpaid debts while write-offs are a final action.

Which is the accounting method for a write off?

Generally Accepted Accounting Principles (GAAP) detail the accounting entries required for a write-off. The two most common business accounting methods for write-offs include the direct write-off method and the allowance method. The entries used will usually vary depending on each individual scenario.