What is the beta of the two stocks?

Joseph Russell

Joseph Russell

Say a company has a beta of 2. This means it is two times as volatile as the overall market. We expect the market overall to go up by 10%. That means this stock could rise by 20%.

How is beta calculated?

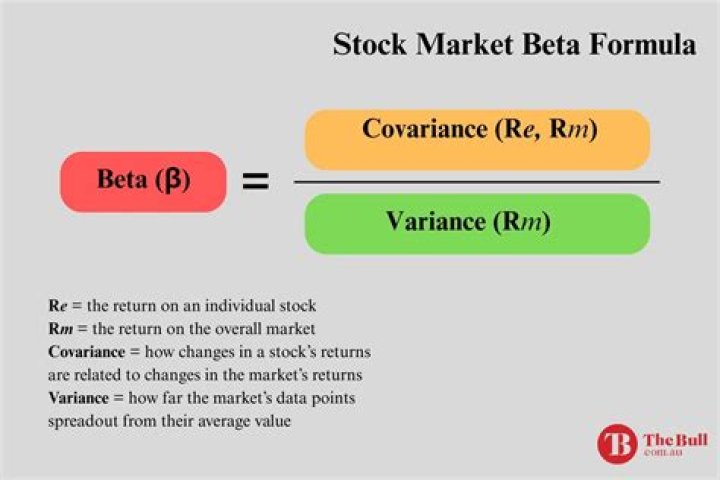

A security’s beta is calculated by dividing the product of the covariance of the security’s returns and the market’s returns by the variance of the market’s returns over a specified period. The beta calculation is used to help investors understand whether a stock moves in the same direction as the rest of the market.

How is beta calculated in CAPM?

Beta is calculated by regressing the percentage change in stock prices versus the percentage change in the overall stock market. CAPM Beta calculation can be done very easily on excel.

How do you calculate the beta of two stocks in a portfolio?

Take the percentage figures and multiply them with each stock’s beta value. For example, if 25% of your portfolio comprises of Apple and it has a beta of 1.43, its weighted beta would amount to 0.3575. Add up the weighted beta figures and that gives you your portfolio beta.

What is a good beta value?

A beta greater than 1.0 suggests that the stock is more volatile than the broader market, and a beta less than 1.0 indicates a stock with lower volatility. Beta is probably a better indicator of short-term rather than long-term risk.

What is the difference between levered and unlevered beta?

Levered beta measures the risk of a firm with debt and equity in its capital structure to the volatility of the market. The other type of beta is known as unlevered beta. Comparing companies’ unlevered betas gives an investor clarity on the composition of risk being assumed when purchasing the stock.

What is a good portfolio beta?

A positive beta is associated with a tendency of the portfolio to move in the same direction as the market. Portfolios, however, can also have betas greater than 1.0, such that a portfolio with a beta of +1.25 would be expected to earn 125% of the market’s return and so on.

How do you calculate beta of a security?

Calculating beta using the covariance/variance formula is probably the most common method of calculating the beta of a stock. This formula takes the covariance of the return of the market and the return of the asset and then divides that by the market return’s variance over a given time frame.

Is High beta good?

Beta is a measure of a stock’s volatility in relation to the overall market. High-beta stocks are supposed to be riskier but provide higher return potential; low-beta stocks pose less risk but also lower returns.

What does high beta indicate?

Beta is a measure of a stock’s volatility in relation to the overall market. If a stock moves less than the market, the stock’s beta is less than 1.0. High-beta stocks are supposed to be riskier but provide higher return potential; low-beta stocks pose less risk but also lower returns.

When would you use an asset beta?

Asset beta is used to measure the risk of a security minus the company’s debt. It is best to use asset beta when either a company or an investor wants to measure a company’s performance in relation to the market without the impact of a company’s debt.

How do you interpret a levered beta?

A levered beta greater than positive 1 or less than negative 1 means that it has greater volatility than the market. A levered beta between negative 1 and positive 1 has less volatility than the market.

Is beta better than Alpha?

What’s the Difference Between Alpha and Beta?

| Alpha | Beta |

|---|---|

| Measures investment performance | Measures the volatility of an investment |

| Helps you identify the best performing investment funds | Helps you identify an asset’s volatility |